Explained Simply: Options 102, option pricing, Moo Moo's option price calculator, and the greeks

In this Options 102 for layman, we will discussed about option prices and its component of intrinsic and extrinsic value. We will also discuss about Black-Scholes theory of options pricing and how the greeks affect the option's price. In this post we will use Moo Moo's option price calculator a lot, so after we are done, we will be an expert on how to use Moo Moo's option price calculator. So let's begin ![]()

![]()

If you have not read Options 101 you can start from here

Option price component

A option's pricing is made out of 2 components, and they are the intrinsic and extrinsic value. Extrinsic value is also known as time value. so in short intrinsic value + extrinsic value = option price. Let us understand the 2 terms first.

Intrinsic Value: In simple term, this is the option's "real value", because on expiration this is the only value left. This is the positive difference between the stock price and the strike price.

So for a CALL option, if the strike price of the option is $10 and the stock price is $15, the intrinsic value is $5 ($15 - $10). However, if the strike price of the option is $10 and the stock price is $5, the intrinsic value is $0, because no one will exercise this CALL option. Like why will the buyer exercise the option to buy shares at $10, when they can buy it at $5 right?

For a PUT option, it will be the inverse. If the strike price of the option is $10 and the stock price is $15, the intrinsic value is $0, because no one will exercise this PUT option. Like why will the buyer exercise the option to sell shares at $10, when they can sell it at $15 right? However, if the strike price of the option is $10 and the stock price is $5, the intrinsic value is $5 ($10 - $5).

Extrinsic (Time) Value: In simple term, this is the "hope the option can earn money because we still have time left" value on the option. In Singapore, there is a saying: 有买有希望. Which means got buy, got hope. It is a similar concept, extrinsic value is the amount of money we pay for "hope". The professional calls it time value, layman like me calls it hope value.

Extrinsic value is determined by many factors which we will cover it later in the post. But let me layout a simple way of thinking of extrinsic value. More time, more hope, so cost us more money. Less time, less hope, so it will be cheaper. More volatile stock price, means higher chance to HUAT BIG BIG, so cost us more money. Less volatile stock price, means lower chance to HUAT BIG BIG, so it is cheaper.

Where can we find the option price and the values

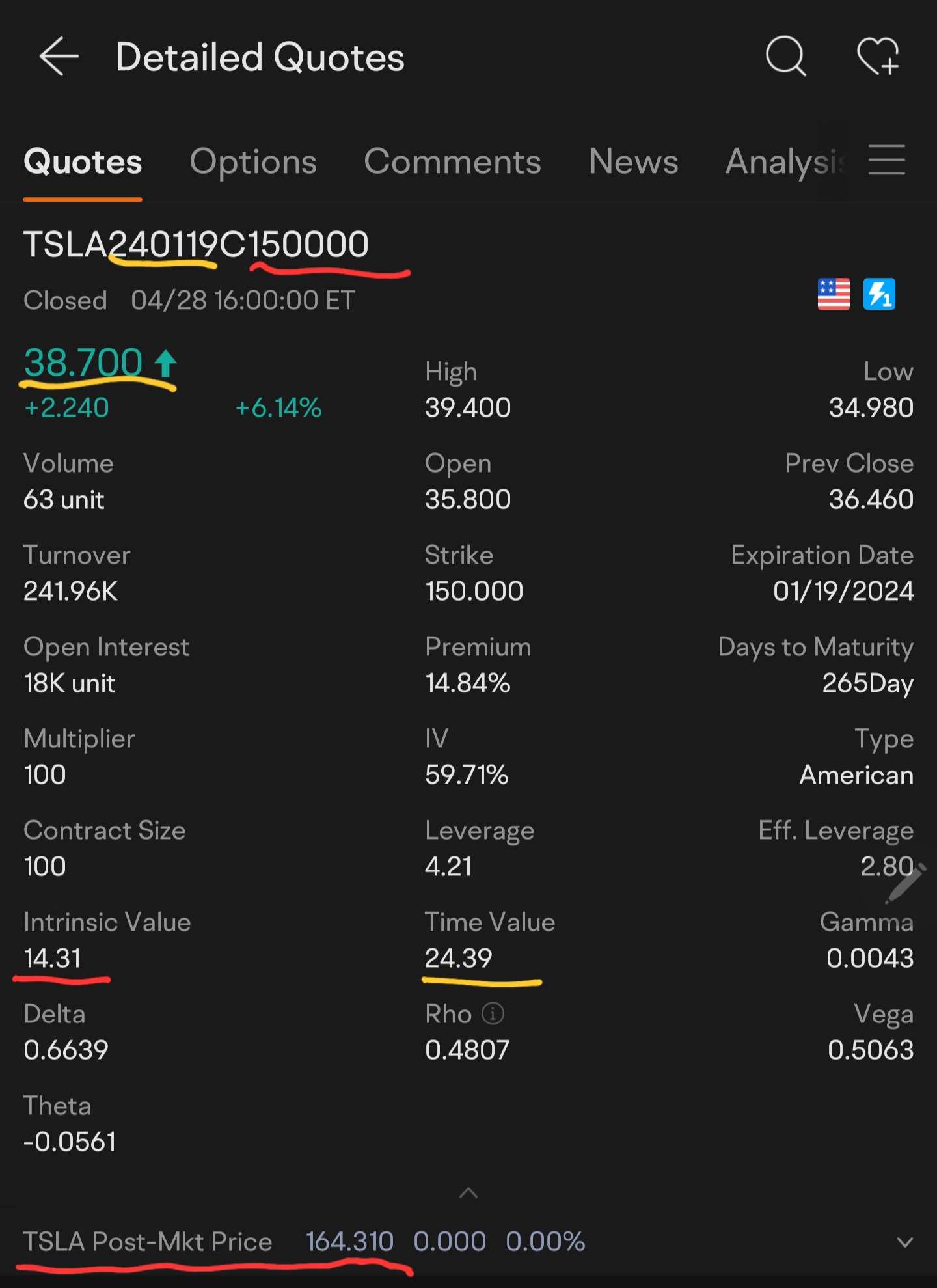

So now let's take a look at a $Tesla(TSLA.US$'s option to find out the pieces that we mentioned about. In the first line, we can see that this is a Tesla CALL option, with a strike price of $150, expiring on 19 Jan 2024.

So now let's take a look at a $Tesla(TSLA.US$'s option to find out the pieces that we mentioned about. In the first line, we can see that this is a Tesla CALL option, with a strike price of $150, expiring on 19 Jan 2024.

Let us first focus on the intrinsic value and their related values which is underlined in red. We can see that the strike price is $150 from the option name. Tesla's current price is $164.31, and the intrinsic value is $14.31 ($164.31 - $150 = $14.31). Why is the intrinsic value $14.31? Because if we exercise the option now, we get to buy Telsa at $150 each, since Tesla is trading at $164.31, that means we can immediately sell the $150 shares for $164.31, earning us $14.31. Therefore, the intrinsic value is $14.31. This is the real value of the option.

Now let's take a look at the extrinsic value (time value) and 1 of the related value which is underlined in yellow. We can see that the time value is $24.39 and the expiry date of the option is 19 Jan 2024. Since the option have so much time left, the time value will be high. When we add the $14.31 in intrinsic value with the $24.39 in extrinsic value, we get $38.70. Which is exactly the option price.

Black-Scholes theory of options pricing and Moo Moo's option price calculator

In the earlier section we said that an option price is made up of intrinsic and extrinsic value. We had discussed how intrinsic value is calculated but we never really go in depth about how extrinsic value is calculated. We said it is a hope value. Real (intrinsic) value + hope (extrinsic) value = option's price. To understand option pricing more in depth, we need to get acquainted with the Black-Scholes option pricing model (Black-Scholes Model: What It Is, How It Works, Options Formula) first. Scholes and Merton won the Nobel prize in Economic Sciences, for developing this model to calculate the theoretical value of an option contract.

In the earlier section we said that an option price is made up of intrinsic and extrinsic value. We had discussed how intrinsic value is calculated but we never really go in depth about how extrinsic value is calculated. We said it is a hope value. Real (intrinsic) value + hope (extrinsic) value = option's price. To understand option pricing more in depth, we need to get acquainted with the Black-Scholes option pricing model (Black-Scholes Model: What It Is, How It Works, Options Formula) first. Scholes and Merton won the Nobel prize in Economic Sciences, for developing this model to calculate the theoretical value of an option contract.

By knowing the stock's current price, the option's strike price, the stock's price volatility, time left on the option and the risk-free interest rate, the model will output a theoretical price for the option contract. The math is as follows

But ain't nobody got time for Math! If we tried to work out the Math on paper or on Excel, the price would have changed because price is moving every seconds. So instead of doing all those Math on paper or on Excel, we can leverage off Moo Moo's option price calculator which does all these Black-Scholes math magic for us. It looks like this:

Under every option's Quotes page, there is this calculator at the bottom. This calculator knows the strike price, it automatically input the current stock price, calculates the current Implied Volatility (IV%) of the stock price and the time left on the option, and sets a default risk-free interest rate. With these values, it automatically calculates the theoretical price for the option. The fair price for the option. If we disagree with the IV or Risk-Free Rate, we can adjust it. If we like to do scenario analysis such as seeing how the option price will fall as time passes, we can adjust it and see the changes to the option price in real-time.

Now that we know that the price of the option is based on the stock's current price, the option's strike price, the stock's price volatility, time left on the option and the risk-free interest rate That would mean that the extrinsic value of an option is also a function of the stock's current price, the option's strike price, the stock's price volatility, time left on the option and the risk-free interest rate.

Let me explain it in layman terms, how those factors affects extrinsic value, which in our case is hope value.

Current stock price & option's strike price: If the strike price and stock price is too far apart, then we would pay lesser to buy hope. Because it is either too hard to win, or too hard to lose. Assume a CALL option, if the stock's price is $20 and the strike price is $100, it is extremely hard for the CALL option to win, so why will we pay more for hope? On the other hand, if the stock's price is $20 and the strike price is $1, it is extremely hard for the CALL option to lose, so why will we pay more for something that is almost guaranteed? Thus, the further apart the stock price and strike price is, the lesser we should pay for hope (extrinsic) value. Which means the closer the the stock price and strike price is the higher the hope (extrinsic) value.

Stock's price volatility: If the stock's price doesn't really move much, maybe like $Gold Trust Ishares(IAU.US$. Then it is less likely that we will win big, so why should we pay so much for hope? The share price might only go up or down by 5%, so why should we big money for a small hope. But if the stock's price is super volatile and can move 50%, 100%, 300% in a year like $NIO Inc(NIO.US$ or $Coinbase(COIN.US$. Then we should be paying more for hope, because we could strike it big.

Time left on the option: This should be quite obvious, if the option expires tomorrow, it is very unlikely that the stock price will move much as compared to an option that expires in a year. So the more time we have, the more hope we have, the more we will pay for hope (extrinsic) value.

Risk-free interest rate: For this, it is more like an opportunity cost. If you buy options, that means that you are losing money as you are not getting the interest. When you sell an option and get money, that means that you are putting the money to get the interest. Thus the model accounts for that so that it is fair for both the seller and the buyer.

the Greeks

Now that we know how options are priced, the next factor to look at is the Greeks. These are the key measurement of risk in the option. Knowing them will allow us to better manage risk. Advance traders could do hedging, like delta hedge, so that they are not affected by the movement of the stock's price. Whether the stock price goes up 1000% or crash to $0, it doesn't affect them. The Greeks are shown in every option chain as follows:

Now that we know how options are priced, the next factor to look at is the Greeks. These are the key measurement of risk in the option. Knowing them will allow us to better manage risk. Advance traders could do hedging, like delta hedge, so that they are not affected by the movement of the stock's price. Whether the stock price goes up 1000% or crash to $0, it doesn't affect them. The Greeks are shown in every option chain as follows:

There are 5 greeks and they are delta, gamma, theta, vega and rho. Now let me explain them simply, with examples.

Delta: Measure the impact to the option's price when the share's price changes. It shows the change in the option's price for every $1 movement in the stock's price. So if we have an option that has a delta of 0.5, that will mean that if the share's price increase by $1, the option's price will increase by $0.50.

Delta is usually used as a proxy to measure the exposure we have with the underlying stock. Which means a delta of 0.5 would mean that holding this 1 option is as though we are hold 50 (0.5 x 100) shares. That is why buying a CALL option or short selling a PUT option have a similar effect to buying the shares. Conversely, a delta of -0.5 would mean that holding this 1 option is as though we short sell 50 (0.5 x 100) shares. That is why buying a PUT option or short selling a CALL option have a similar effect to short selling the shares.

We can use Moo Moo's calculator to see the effect. Let's use this $Microsoft(MSFT.US$'s $315 CALL options expiring 19 Jan 2024 as an example. When the share price is $307.60, the delta of the option is 0.5254. This means that if the share price increased by $1 to $308.60, the option's price will increase by $0.5254. Which means the option's price should go from $29.1213 to $29.6467. However, we see that the option price is $29.6493 instead, close enough but not exactly the same. This is because of gamma, as the share price moved, gamma caused delta to move as well. So there is kind of a double movement. So let's talk about Gamma next.

Gamma: Measures the impact to the option's delta when the share's price changes. It shows the change in the option's delta for every $1 movement in the stock's price. So if an option have a delta of 0.50 and had a Gamma of 0.01, that means that if the share's price increase by $1, the option's delta will increase by 0.01 to 0.51. This is the key greek that we use to create a gamma squeeze. Ryan Cohen leveraged on to create a short squeeze and a gamma squeeze combo on $Bed Bath & Beyond Inc(BBBY.US$, by buying a lot of the $80 CALL options.

Using the earlier's $Microsoft(MSFT.US$ CALL option example. We can see that as the share price increase $1, delta moved by 0.0051, changing from 0.5254 to 0.5305. So gamma caused delta to move, and delta causes option's price to move, there is a chain effect.

Theta: Measure the impact of the movement of time on the option's price. It shows the change in the option's price for every day that has passed. So a theta of -0.5 means that if another day passed, the option's price will decrease by $0.50. Option's sellers loves theta, as it is the only thing that gives a guaranteed revenue. Time value will 100% go to 0 after expiry, so sellers are guaranteed 100% to earn from theta (but seller can lose due to other factors). Thus, there are a whole community of option sellers that have banded together and called themselves the theta gang ![]()

Using Moo Moo's calculator to see the effect of theta on $Invesco QQQ Trust(QQQ.US$'s $322 PUT options expiring 4 May 2023 as an example. When the share price is $322.82 and there are 5 days left on the option, the theta of the option is -0.2696. This means that once one day has passed, we will see the option's price decrease by $0.2696, the option price will drop from $2.7381 to $2.4685.

One thing to note is that theta burn will increase more and more as it gets closer to expiry. Theta burn will start to increase exponentially once there are only 30 days left on the option. Thus, a lot of option seller like to sell option that is close to expiration, to burn time value faster and earn from it.

Vega: Measure the impact on the option's price when implied volatility (IV%) changes. It shows the change in the option's price for every 1% movement in implied volatility (IV%). So a vega of 0.5 means that if the implied volatility (IV%) increase by 1%, the option's price will increase by $0.50. This is the key greek that we use to find trades that is ready for a IV crush ![]()

![]()

Using Moo Moo's calculator to see the effect of vega on $Palantir(PLTR.US$'s $8 PUT options expiring 19 Jan 2024 as an example. When the share price is $7.78, and the vega of the option is 0.0261. This means that if the IV increased by 1%, from 51% to 52%, we will see the option's price increase by $0.0261. Rising to $1.4668 from $1.4407.

Rho: Measure the impact to the option's price when interest rate changes. It shows the change in the option's price for every 1% movement in interest rate. So a rho of 0.5 means that if interest rate increase by 1%, the option's price will increase by $0.50. But this greeks aren't really as significant as the others.

We can use Moo Moo's calculator to see the effect too. Let's use this $SPDR S&P 500 ETF(SPY.US$'s $415 CALL options expiring 4 May 2023 as an example. When the share price is $416.18, the rho of the option is 0.0378. This means that if the interest rate increased by 1% to 2%, the option's price will increase by $0.0378. Which means the option's price should go from $4.0613 to $4.0991. However, we can see that there is some tiny difference in the expected price and the calculator's price. That is negligible and is caused by the model calculation methodology, so don't worry about it.

Scenario Analysis using Moo Moo's options calculator

So now that we know how to use Moo Moo's option calculator to adjust important factors to see the change in the option's price. We can use the calculator to perform scenario analysis to see what will happen to our option in different scenario. Let me show you an example of how we can do some simple scenario analysis using $Alibaba(BABA.US$'s $85 CALL option expiring 19 Jan 2024.

So now that we know how to use Moo Moo's option calculator to adjust important factors to see the change in the option's price. We can use the calculator to perform scenario analysis to see what will happen to our option in different scenario. Let me show you an example of how we can do some simple scenario analysis using $Alibaba(BABA.US$'s $85 CALL option expiring 19 Jan 2024.

We know that Chinese's stocks had crashed for the past 2 years, and there is a chance that it could rally. But it could also not move at all. So before we make any options trade, we can make some assumptions for the different possible scenarios, and analyse the impact of it.

So if we assume a bull case and assume that $Alibaba(BABA.US$ will go up to $130 on 1 Sept 2023, which would also cause an increase in volatility. We can input our assumptions into the price calculator to get the theoretical option price. What we can see that in a bull case, our $14.1198 option would be valued at $47.7311 on 1 Sept, that is a gain of 238%.

However, if we assume in another case where $Alibaba(BABA.US$ might not really move at all on 1 Sept 2023. We can input those assumptions into the price calculator to get the theoretical option price. What we can see is that our $14.1198 option would be valued at $10.2495 on 1 Sept, which is a loss of 27.4%.

Using Moo Moo's price calculator, it will allow us to evaluate the risk and rewards based on our assumptions, and give us a clear idea if what we are going to do is a smart move or not.

Conclusion

Now that we have learnt more about options and Moo Moo's option price calculator tool, we can use them wisely in our trade so that we do not make silly mistakes. Like setting up an impossible to win option trade, or having a trade that gives us little reward but taking huge risks.

Now that we have learnt more about options and Moo Moo's option price calculator tool, we can use them wisely in our trade so that we do not make silly mistakes. Like setting up an impossible to win option trade, or having a trade that gives us little reward but taking huge risks.

That concludes our 102 class, and if you like to learn more about the difference between In The Money (ITM), At The Money (ATM), and Out of The Money (OTM) options, and the risk reward profile for each of them. You can check out the Option 103 post here: Explained Simply: Options 103, ITM ATM & OTM; Risk, Reward and Strategy.

You could also join Moo Moo's option group chatroom too, to have more in depth discussion or simply to ask questions ![]()

![]() Just search options, click on groups and here are the 3 options group chat in Moo Moo

Just search options, click on groups and here are the 3 options group chat in Moo Moo

Disclaimer: Community is offered by Moomoo Technologies Inc. and is for educational purposes only.

Read more

Comment

Sign in to post a comment

Moo Contributor

crawled out of poverty, working towards FIRE!! (financial independence, retired early)

14KFollowers

104Following

16KVisitors

Follow

Syuee :

MonkeyGee : like always wonderful content

doctorpot1OP MonkeyGee: thank you hope it had been useful to you

hope it had been useful to you

rennymc : Awesome info! You should be the moomoo staff writer about options. Thank you for this!

doctorpot1OP rennymc: no problem glad it helps

glad it helps