If you're looking for a multi-bagger, there's a few things to keep an eye out for. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. In light of that, when we looked at HKT Trust and HKT (HKG:6823) and its ROCE trend, we weren't exactly thrilled.

What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for HKT Trust and HKT:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.081 = HK$7.1b ÷ (HK$110b - HK$21b) (Based on the trailing twelve months to June 2022).

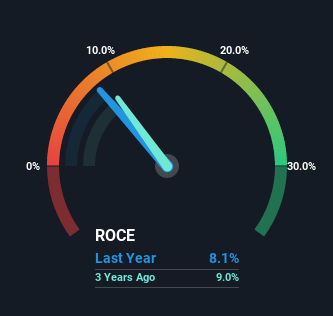

Therefore, HKT Trust and HKT has an ROCE of 8.1%. On its own that's a low return, but compared to the average of 6.6% generated by the Telecom industry, it's much better.

View our latest analysis for HKT Trust and HKT

SEHK:6823 Return on Capital Employed November 2nd 2022

SEHK:6823 Return on Capital Employed November 2nd 2022Above you can see how the current ROCE for HKT Trust and HKT compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering HKT Trust and HKT here for free.

How Are Returns Trending?

Things have been pretty stable at HKT Trust and HKT, with its capital employed and returns on that capital staying somewhat the same for the last five years. Businesses with these traits tend to be mature and steady operations because they're past the growth phase. So don't be surprised if HKT Trust and HKT doesn't end up being a multi-bagger in a few years time. That probably explains why HKT Trust and HKT has been paying out 116% of its earnings as dividends to shareholders. These mature businesses typically have reliable earnings and not many places to reinvest them, so the next best option is to put the earnings into shareholders pockets.

The Bottom Line

In a nutshell, HKT Trust and HKT has been trudging along with the same returns from the same amount of capital over the last five years. Unsurprisingly, the stock has only gained 26% over the last five years, which potentially indicates that investors are accounting for this going forward. So if you're looking for a multi-bagger, the underlying trends indicate you may have better chances elsewhere.

One final note, you should learn about the 2 warning signs we've spotted with HKT Trust and HKT (including 1 which shouldn't be ignored) .

While HKT Trust and HKT may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.