Unfortunately for shareholders, when Brockman Mining Limited (HKG:159) reported results for the period to June 2022, its auditors, Ernst & Young LLP, expressed uncertainty about whether it can continue as a going concern. Thus we can say that, based on the results to that date, the company should raise capital or otherwise raise cash, without much delay.

Since the company probably needs cash fairly quickly, it may be in a position where it has to accept whatever terms it can get. So current risks on the balance sheet could have a big impact on how shareholders fare from here. The big consideration is whether it can repay its debt, since in the worst case scenario, creditors could force the company to bankruptcy.

See our latest analysis for Brockman Mining

What Is Brockman Mining's Debt?

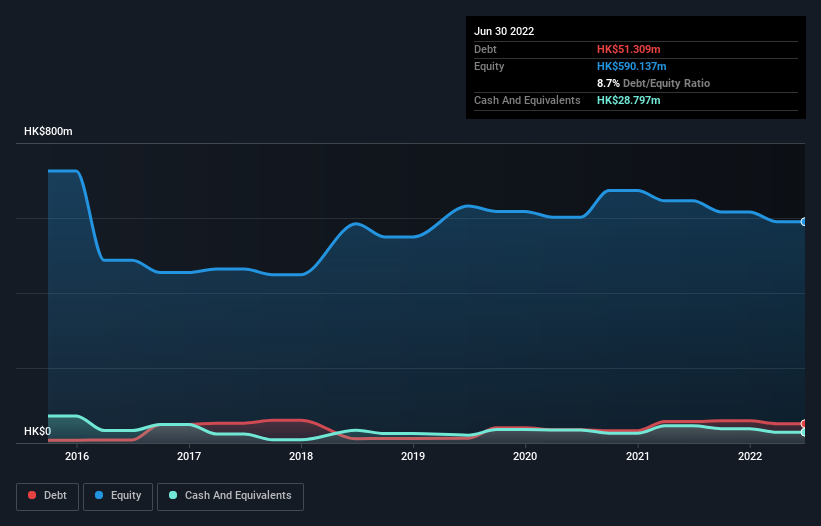

As you can see below, Brockman Mining had HK$51.3m of debt at June 2022, down from HK$57.2m a year prior. On the flip side, it has HK$28.8m in cash leading to net debt of about HK$22.5m.

As you can see below, Brockman Mining had HK$51.3m of debt at June 2022, down from HK$57.2m a year prior. On the flip side, it has HK$28.8m in cash leading to net debt of about HK$22.5m.

SEHK:159 Debt to Equity History September 25th 2022

SEHK:159 Debt to Equity History September 25th 2022How Strong Is Brockman Mining's Balance Sheet?

The latest balance sheet data shows that Brockman Mining had liabilities of HK$16.3m due within a year, and liabilities of HK$158.8m falling due after that. Offsetting this, it had HK$28.8m in cash and HK$21.0k in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$146.3m.

Given Brockman Mining has a market capitalization of HK$1.70b, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. But either way, Brockman Mining has virtually no net debt, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is Brockman Mining's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Given its lack of meaningful operating revenue, investors are probably hoping that Brockman Mining finds some valuable resources, before it runs out of money.

Caveat Emptor

Importantly, Brockman Mining had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at HK$40m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled HK$20m in negative free cash flow over the last twelve months. So suffice it to say we do consider the stock to be risky. We're too cautious to want to invest in a company after an auditor has expressed doubts about its ability to continue as a going concern. That's because we find it more comfortable to invest in companies that always keep the balance sheet reasonably strong. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for Brockman Mining you should be aware of, and 1 of them doesn't sit too well with us.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.