If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Having said that, from a first glance at Intco Medical Technology (SZSE:300677) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Intco Medical Technology is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.099 = CN¥1.8b ÷ (CN¥21b - CN¥2.2b) (Based on the trailing twelve months to June 2022).

0.099 = CN¥1.8b ÷ (CN¥21b - CN¥2.2b) (Based on the trailing twelve months to June 2022).

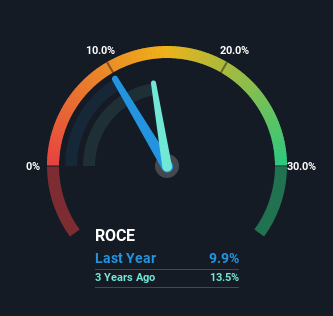

So, Intco Medical Technology has an ROCE of 9.9%. On its own that's a low return on capital but it's in line with the industry's average returns of 10%.

See our latest analysis for Intco Medical Technology

SZSE:300677 Return on Capital Employed September 16th 2022

SZSE:300677 Return on Capital Employed September 16th 2022Historical performance is a great place to start when researching a stock so above you can see the gauge for Intco Medical Technology's ROCE against it's prior returns. If you're interested in investigating Intco Medical Technology's past further, check out this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

When we looked at the ROCE trend at Intco Medical Technology, we didn't gain much confidence. Over the last five years, returns on capital have decreased to 9.9% from 21% five years ago. And considering revenue has dropped while employing more capital, we'd be cautious. This could mean that the business is losing its competitive advantage or market share, because while more money is being put into ventures, it's actually producing a lower return - "less bang for their buck" per se.

On a related note, Intco Medical Technology has decreased its current liabilities to 10% of total assets. That could partly explain why the ROCE has dropped. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.

The Key Takeaway

We're a bit apprehensive about Intco Medical Technology because despite more capital being deployed in the business, returns on that capital and sales have both fallen. Yet despite these poor fundamentals, the stock has gained a huge 162% over the last five years, so investors appear very optimistic. In any case, the current underlying trends don't bode well for long term performance so unless they reverse, we'd start looking elsewhere.

If you want to know some of the risks facing Intco Medical Technology we've found 3 warning signs (1 doesn't sit too well with us!) that you should be aware of before investing here.

While Intco Medical Technology may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.