The harsh reality for Logan Group Company Limited (HKG:3380) shareholders is that its auditors, UniTax Prism CPA Limited, expressed doubts about its ability to continue as a going concern, in its reported results to June 2022. It is therefore fair to assume that, based on those financials, the company should strengthen its balance sheet in the short term, perhaps by issuing shares.

Given its situation, it may not be in a good position to raise capital on favorable terms. So shareholders should absolutely be taking a close look at how risky the balance sheet is. The big consideration is whether it can repay its debt, since in the worst case scenario, creditors could force the company to bankruptcy.

See our latest analysis for Logan Group

What Is Logan Group's Debt?

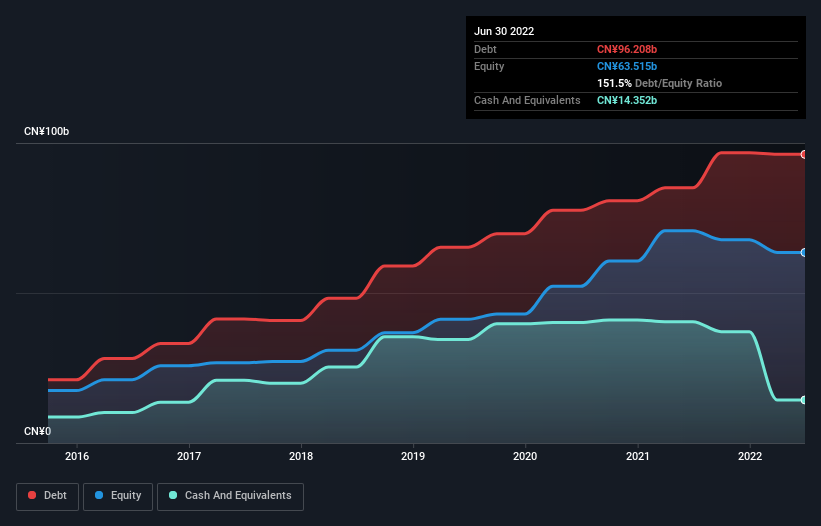

As you can see below, at the end of June 2022, Logan Group had CN¥96.2b of debt, up from CN¥85.1b a year ago. Click the image for more detail. However, it also had CN¥14.4b in cash, and so its net debt is CN¥81.9b.

SEHK:3380 Debt to Equity History September 12th 2022

SEHK:3380 Debt to Equity History September 12th 2022How Healthy Is Logan Group's Balance Sheet?

We can see from the most recent balance sheet that Logan Group had liabilities of CN¥172.6b falling due within a year, and liabilities of CN¥58.0b due beyond that. On the other hand, it had cash of CN¥14.4b and CN¥53.2b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥163.1b.

This deficit casts a shadow over the CN¥3.87b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Logan Group would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

As it happens Logan Group has a fairly concerning net debt to EBITDA ratio of 13.9 but very strong interest coverage of 12.6. So either it has access to very cheap long term debt or that interest expense is going to grow! Shareholders should be aware that Logan Group's EBIT was down 64% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Logan Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Logan Group reported free cash flow worth 10% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

On the face of it, Logan Group's EBIT growth rate left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But at least it's pretty decent at covering its interest expense with its EBIT; that's encouraging. Taking into account all the aforementioned factors, it looks like Logan Group has too much debt. That sort of riskiness is ok for some, but it certainly doesn't float our boat. While some investors may specialize in these sort of situations, it's simply too risky and complicated for us to want to invest in a company after an auditor has expressed doubts about its ability to continue as a going concern. Our preference is to invest in companies that always make sure the auditor has confidence that the company will continue as a going concern. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 4 warning signs for Logan Group you should be aware of, and 2 of them are concerning.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.