ESR Group Limited's (HKG:1821) stock performed strongly after the recent earnings report. Despite this, we feel that there are some reasons to be cautious with these earnings.

Check out our latest analysis for ESR Group

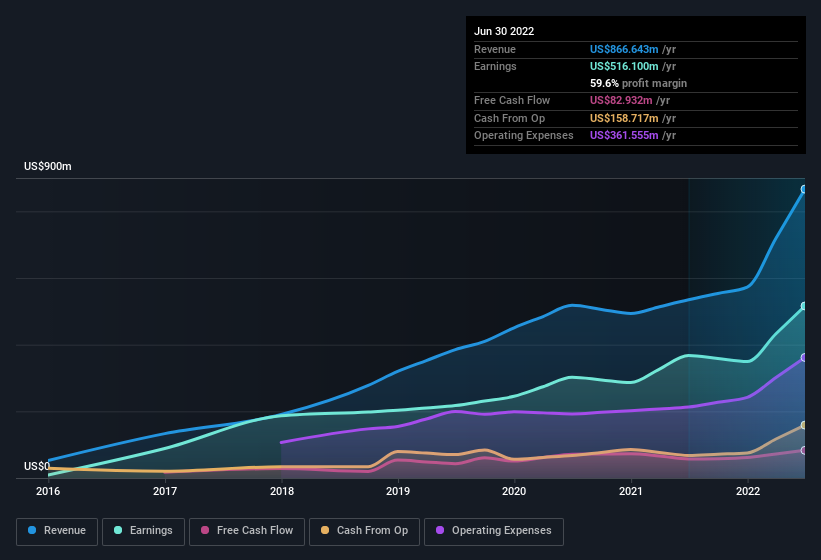

SEHK:1821 Earnings and Revenue History September 1st 2022

SEHK:1821 Earnings and Revenue History September 1st 2022To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. As it happens, ESR Group issued 43% more new shares over the last year. As a result, its net income is now split between a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. You can see a chart of ESR Group's EPS by clicking here.

How Is Dilution Impacting ESR Group's Earnings Per Share (EPS)?

As you can see above, ESR Group has been growing its net income over the last few years, with an annualized gain of 137% over three years. But EPS was only up 70% per year, in the exact same period. And at a glance the 40% gain in profit over the last year impresses. But in comparison, EPS only increased by 14% over the same period. And so, you can see quite clearly that dilution is having a rather significant impact on shareholders.

In the long term, earnings per share growth should beget share price growth. So it will certainly be a positive for shareholders if ESR Group can grow EPS persistently. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Our data indicates that ESR Group insiders have been buying shares! Luckily we are in a position to provide you with this free chart of of all insider buying (and selling).

The Impact Of Unusual Items On Profit

Finally, we should also consider the fact that unusual items boosted ESR Group's net profit by US$315m over the last year. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. Which is hardly surprising, given the name. We can see that ESR Group's positive unusual items were quite significant relative to its profit in the year to June 2022. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On ESR Group's Profit Performance

In its last report ESR Group benefitted from unusual items which boosted its profit, which could make the profit seem better than it really is on a sustainable basis. On top of that, the dilution means that its earnings per share performance is worse than its profit performance. Considering all this we'd argue ESR Group's profits probably give an overly generous impression of its sustainable level of profitability. If you'd like to know more about ESR Group as a business, it's important to be aware of any risks it's facing. For example, we've discovered 2 warning signs that you should run your eye over to get a better picture of ESR Group.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.