It's been a pretty great week for Vital Farms, Inc. (NASDAQ:VITL) shareholders, with its shares surging 15% to US$13.54 in the week since its latest quarterly results. It was overall a positive result, with revenues beating expectations by 4.1% to hit US$83m. Vital Farms also reported a statutory profit of US$0.0047, which was a nice improvement from the loss that the analysts were predicting. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

See our latest analysis for Vital Farms

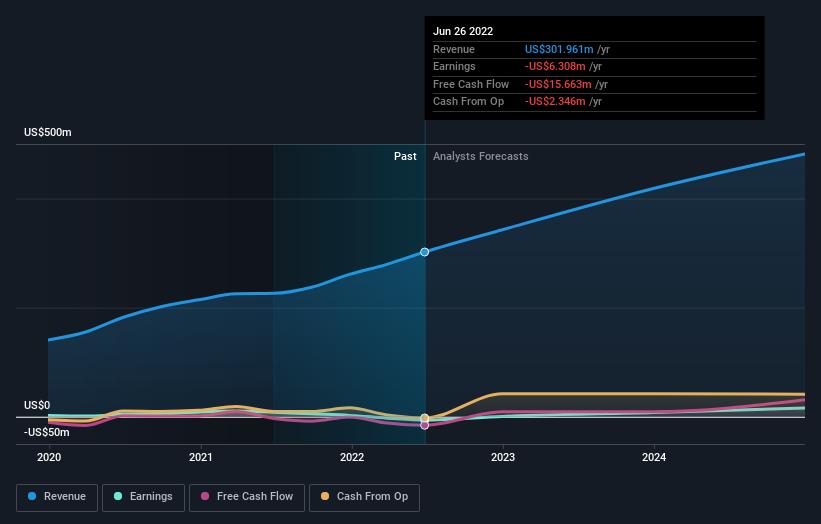

NasdaqGM:VITL Earnings and Revenue Growth August 7th 2022

NasdaqGM:VITL Earnings and Revenue Growth August 7th 2022Following the latest results, Vital Farms' seven analysts are now forecasting revenues of US$342.8m in 2022. This would be a decent 14% improvement in sales compared to the last 12 months. Earnings are expected to improve, with Vital Farms forecast to report a statutory profit of US$0.02 per share. Before this earnings report, the analysts had been forecasting revenues of US$342.7m and earnings per share (EPS) of US$0.038 in 2022. The analysts seem to have become more bearish following the latest results. While there were no changes to revenue forecasts, there was a large cut to EPS estimates.

The consensus price target held steady at US$17.21, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values Vital Farms at US$23.00 per share, while the most bearish prices it at US$14.00. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Vital Farms' past performance and to peers in the same industry. We can infer from the latest estimates that forecasts expect a continuation of Vital Farms'historical trends, as the 29% annualised revenue growth to the end of 2022 is roughly in line with the 33% annual revenue growth over the past year. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 2.5% per year. So it's pretty clear that Vital Farms is forecast to grow substantially faster than its industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Vital Farms. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. The consensus price target held steady at US$17.21, with the latest estimates not enough to have an impact on their price targets.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Vital Farms going out to 2024, and you can see them free on our platform here..

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.