It is hard to get excited after looking at Scholastic's (NASDAQ:SCHL) recent performance, when its stock has declined 22% over the past three months. However, stock prices are usually driven by a company's financials over the long term, which in this case look pretty respectable. Particularly, we will be paying attention to Scholastic's ROE today.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for Scholastic

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Scholastic is:

5.1% = US$60m ÷ US$1.2b (Based on the trailing twelve months to August 2022).

The 'return' is the profit over the last twelve months. So, this means that for every $1 of its shareholder's investments, the company generates a profit of $0.05.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

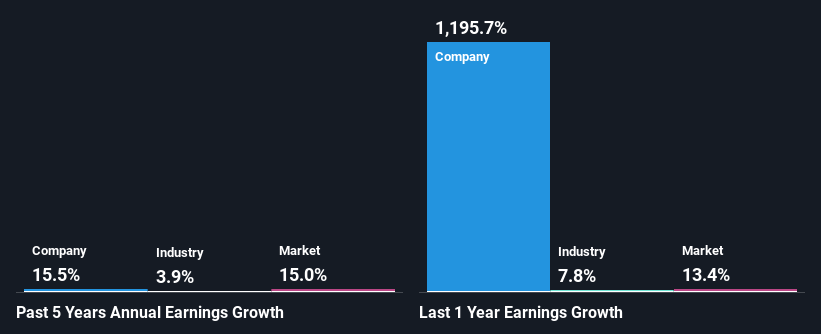

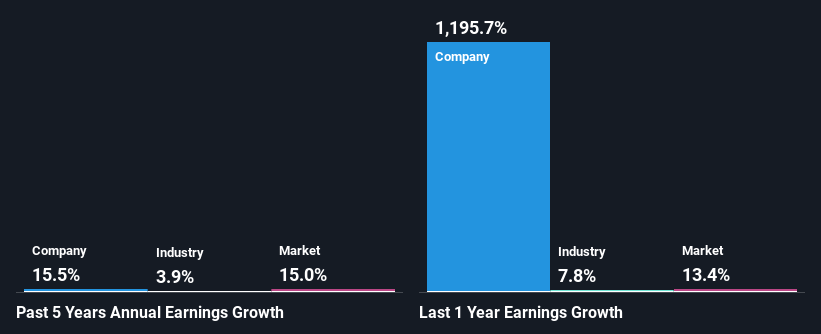

A Side By Side comparison of Scholastic's Earnings Growth And 5.1% ROE

At first glance, Scholastic's ROE doesn't look very promising. Next, when compared to the average industry ROE of 14%, the company's ROE leaves us feeling even less enthusiastic. Scholastic was still able to see a decent net income growth of 16% over the past five years. So, there might be other aspects that are positively influencing the company's earnings growth. Such as - high earnings retention or an efficient management in place.

We then compared Scholastic's net income growth with the industry and we're pleased to see that the company's growth figure is higher when compared with the industry which has a growth rate of 3.9% in the same period.

NasdaqGS:SCHL Past Earnings Growth October 24th 2022

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It's important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is Scholastic fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Scholastic Making Efficient Use Of Its Profits?

Scholastic has a healthy combination of a moderate three-year median payout ratio of 26% (or a retention ratio of 74%) and a respectable amount of growth in earnings as we saw above, meaning that the company has been making efficient use of its profits.

Additionally, Scholastic has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders.

Conclusion

On the whole, we do feel that Scholastic has some positive attributes. Even in spite of the low rate of return, the company has posted impressive earnings growth as a result of reinvesting heavily into its business. While we won't completely dismiss the company, what we would do, is try to ascertain how risky the business is to make a more informed decision around the company. You can see the 1 risk we have identified for Scholastic by visiting our risks dashboard for free on our platform here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

ナスダック(Scholastic)(株式コード:SCCL)の最近の表現を見て、興奮しにくく、その株価は過去3カ月で22%下落した。しかし、株価は通常、会社の長期財務状況によって推進されており、この場合、財務状況はかなり良いように見える。特に,我々は今日Scholasticの純資産収益率(ROE)に注目する

純資産収益率、すなわち株式収益率は、ある会社が株主から投資リターンを得る有効度を評価する有用なツールである。簡単に言うと、それはその資本資本に対する会社の収益性を評価するために使用される

Scholasticの最新の分析を見てみましょう

純資産収益率はどのように計算されますか

それは..株式収益率公式はい:

株式収益率=(継続経営の)純利益?株主権益

以上の式によると、学術会社の純資産収益率は以下のようになる

5.1%=6000万ドル×12億ドル(2022年8月までの12カ月の過去実績に基づく)。

“収益”は過去12ヶ月の利益だ。したがって、これは株主が1ドル投資するごとに、会社が0.05ドルの利益を生むことを意味する

なぜ純資産収益率は収益増加に重要なのですか

これまで、純資産収益率はある会社の収益性を測る指標であることが分かった。会社が再投資や“保留”のどれだけの利益を選択するかによって、1つの会社が将来利益を生み出す能力を評価することができる。他の条件が同じであると仮定すると,同じ特徴を持たない会社よりも高い株式収益率とより高い利益保持率を持つ会社は通常より高い成長率を持つことになる

Scholastic収益率と5.1%純資産収益率の並列比較

一見、Scholasticの純資産収益率はあまり有望ではないように見える。次に、14%の業界平均純資産収益率に比べて、同社の純資産収益率はより不親切を感じている。この5年間、Scholasticは16%の相当な純収入増加を見ることができた。したがって、会社の収益増加に積極的に影響を与えている他の側面があるかもしれない。例えば、高い収益が維持されているか、または効果的に管理されている

そして,Scholasticの純収入増加を業界と比較したところ,同期の3.9%の業界成長率よりも同社の方が増加率が高いことが分かった

NasdaqGS:Schlの過去の収益増加2022年10月24日

会社に価値を与える基礎はその利益成長に大きくリンクしている。投資家にとって重要なのは、市場が会社の予想した収益増加(または低下)を消化したかどうかを知ることだ。そうすることで、彼らは株が澄んだ青い水域に入るのか、沼の水域に入るのかを知るだろう。他の会社と比較して、学術会社の価値は公平ですか?この3つの評価指標はあなたが決定するのに役立つかもしれない

学術グループは利益を有効に利用していますか

私たちが上で見たように、Scholasticは26%の適度な3年間中央値配当率(または74%の保留率)と相当な収益増加の健康的な組み合わせを持っており、これは同社がその利益を有効に利用してきたことを意味する

さらに、Scholasticは少なくとも10年間配当金を支払っており、これは同社が株主と利益を非常に真剣に共有していることを意味する

結論.結論

全体的に、私たちはScholasticがいくつかの肯定的な属性を持っていると思う。収益率は低いにもかかわらず、業務に大量の再投資を行ったため、同社は印象的な収益増加を実現した。私たちはこの会社を完全に解雇するわけではありませんが、私たちがすべきことは、この業務が会社の周りでより賢明な決定を下すリスクがどれだけ大きいかを確認することです。私たちを訪問することでリスクコントロールパネル私たちのプラットフォームでは無料です

この文章に何かフィードバックはありますか。内容が心配ですか。 連絡を取り合う私たちに直接連絡します。あるいは,編集グループに電子メールを送信することも可能であり,アドレスはimplywallst.comである.

本稿ではSimply Wall St.によって作成され,包括的である私たちは歴史データとアナリスト予測に基づくコメントを偏りのない方法で提供するだけで、私たちの文章は財務アドバイスとしてのつもりはありません。それは株を売買する提案にもなりませんし、あなたの目標やあなたの財務状況も考慮していません。私たちの目標はあなたにファンダメンタルデータによって駆動される長期的な重点分析をもたらすことです。私たちの分析は最新の価格に敏感な会社の公告や定性材料を考慮しないかもしれないことに注意してください。Simply Wall St.上記のいずれの株に対しても在庫を持っていない.