-

市场

-

产品

-

资讯

-

Moo社区

-

课堂

-

查看更多

-

功能介绍

-

费用费用透明,无最低余额限制

投资选择、功能介绍、费用相关信息由Moomoo Financial Inc.提供

- English

- 中文繁體

- 中文简体

- 深色

- 浅色

There's Been No Shortage Of Growth Recently For Warner Music Group's (NASDAQ:WMG) Returns On Capital

There's Been No Shortage Of Growth Recently For Warner Music Group's (NASDAQ:WMG) Returns On Capital

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, we've noticed some promising trends at Warner Music Group (NASDAQ:WMG) so let's look a bit deeper.

Return On Capital Employed (ROCE): What Is It?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Warner Music Group:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.16 = US$717m ÷ (US$7.8b - US$3.4b) (Based on the trailing twelve months to September 2022).

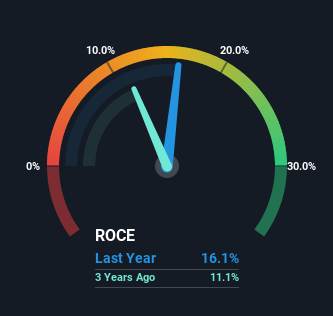

So, Warner Music Group has an ROCE of 16%. On its own, that's a standard return, however it's much better than the 8.4% generated by the Entertainment industry.

See our latest analysis for Warner Music Group

Above you can see how the current ROCE for Warner Music Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

What Does the ROCE Trend For Warner Music Group Tell Us?

The trends we've noticed at Warner Music Group are quite reassuring. Over the last five years, returns on capital employed have risen substantially to 16%. Basically the business is earning more per dollar of capital invested and in addition to that, 23% more capital is being employed now too. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

On a side note, Warner Music Group's current liabilities are still rather high at 43% of total assets. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Bottom Line On Warner Music Group's ROCE

All in all, it's terrific to see that Warner Music Group is reaping the rewards from prior investments and is growing its capital base. Given the stock has declined 17% in the last year, this could be a good investment if the valuation and other metrics are also appealing. So researching this company further and determining whether or not these trends will continue seems justified.

If you want to know some of the risks facing Warner Music Group we've found 3 warning signs (1 is a bit unpleasant!) that you should be aware of before investing here.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

如果我们想要找到一只可以长期成倍增长的股票,我们应该寻找什么潜在趋势?通常,我们会注意到一种增长的趋势退货关于已使用资本(ROCE)以及与之相伴随的是不断扩大的基地已动用资本的比例。如果你看到这个,通常意味着它是一家拥有出色商业模式和大量有利可图的再投资机会的公司。考虑到这一点,我们在以下方面注意到一些有希望的趋势华纳音乐集团纳斯达克:WMG)所以让我们看得更深入一些。

资本回报率(ROCE):它是什么?

如果你以前没有使用过ROCE,它衡量的是一家公司从业务资本中获得的“回报”(税前利润)。分析师使用以下公式来计算华纳音乐集团的股价:

已动用资本回报率=息税前收益(EBIT)?(总资产-流动负债)

0.16美元=7.17亿美元(78亿美元-34亿美元)(基于截至2022年9月的过去12个月)。

所以,华纳音乐集团的净资产收益率为16%。就其本身而言,这是一个标准回报率,但比娱乐业8.4%的回报率要好得多。

查看我们对华纳音乐集团的最新分析

在上面,你可以看到华纳音乐集团目前的净资产收益率与之前的资本回报率相比如何,但你只能从过去知道这么多。如果您感兴趣,您可以在我们的免费分析师对该公司的预测报告。

华纳音乐集团的ROCE趋势告诉了我们什么?

我们在华纳音乐集团注意到的趋势相当令人放心。过去五年,已动用资本回报率大幅上升至16%。基本上,企业每投入一美元资本就能赚到更多的钱,除此之外,现在使用的资本也增加了23%。这可能表明,有很多机会在内部以更高的利率进行资本投资,这种组合在多头投资者中很常见。

另外,华纳音乐集团目前的负债仍相当高,占总资产的43%。这实际上意味着供应商(或短期债权人)正在为很大一部分业务提供资金,因此只需意识到这可能会带来一些风险因素。理想情况下,我们希望看到这一比例降低,因为这将意味着承担风险的债务更少。

华纳音乐集团ROCE的底线

总而言之,很高兴看到华纳音乐集团从之前的投资中获得了回报,并正在扩大其资本基础。鉴于该公司股价在过去一年中下跌了17%,如果估值和其他指标也具有吸引力,这可能是一笔不错的投资。因此,进一步研究这家公司,并确定这些趋势是否会继续下去似乎是合理的。

如果你想知道华纳音乐集团面临的一些风险,我们找到了3个警示标志(1有点令人不快!)在这里投资之前你应该意识到这一点。

如果你想寻找收入丰厚的可靠公司,看看这个免费拥有良好资产负债表和可观股本回报率的公司名单。

对这篇文章有什么反馈吗?担心内容吗?保持联系直接与我们联系。或者,也可以给编辑组发电子邮件,地址是implywallst.com。

本文由Simply Wall St.撰写,具有概括性。我们仅使用不偏不倚的方法提供基于历史数据和分析师预测的评论,我们的文章并不打算作为财务建议。它不构成买卖任何股票的建议,也没有考虑你的目标或你的财务状况。我们的目标是为您带来由基本面数据驱动的长期重点分析。请注意,我们的分析可能不会将最新的对价格敏感的公司公告或定性材料考虑在内。Simply Wall St.对上述任何一只股票都没有持仓。

moomoo是Moomoo Technologies Inc.公司提供的金融信息和交易应用程序。

在美国,moomoo上的投资产品和服务由Moomoo Financial Inc.提供,一家受美国证券交易委员会(SEC)监管的持牌主体。 Moomoo Financial Inc.是金融业监管局(FINRA)和证券投资者保护公司(SIPC)的成员。

在新加坡,moomoo上的投资产品和服务是通过Moomoo Financial Singapore Pte. Ltd.提供,该公司受新加坡金融管理局(MAS)监管(牌照号码︰CMS101000) ,持有资本市场服务牌照 (CMS) ,持有财务顾问豁免(Exempt Financial Adviser)资质。本内容未经新加坡金融管理局的审查。

在澳大利亚,moomoo上的金融产品和服务是通过Futu Securities (Australia) Ltd提供,该公司是受澳大利亚证券和投资委员会(ASIC)监管的澳大利亚金融服务许可机构(AFSL No. 224663)。请阅读并理解我们的《金融服务指南》、《条款与条件》、《隐私政策》和其他披露文件,这些文件可在我们的网站 https://www.moomoo.com/au中获取。

在加拿大,通过moomoo应用提供的仅限订单执行的券商服务由Moomoo Financial Canada Inc.提供,并受加拿大投资监管机构(CIRO)监管。

在马来西亚,moomoo上的投资产品和服务是通过Moomoo Securities Malaysia Sdn. Bhd. 提供,该公司受马来西亚证券监督委员会(SC)监管(牌照号码︰eCMSL/A0397/2024) ,持有资本市场服务牌照 (CMSL) 。本内容未经马来西亚证券监督委员会的审查。

Moomoo Technologies Inc., Moomoo Financial Inc., Moomoo Financial Singapore Pte. Ltd., Futu Securities (Australia) Ltd, Moomoo Financial Canada Inc.,和Moomoo Securities Malaysia Sdn. Bhd.是关联公司。

风险及免责提示

moomoo是Moomoo Technologies Inc.公司提供的金融信息和交易应用程序。

在美国,moomoo上的投资产品和服务由Moomoo Financial Inc.提供,一家受美国证券交易委员会(SEC)监管的持牌主体。 Moomoo Financial Inc.是金融业监管局(FINRA)和证券投资者保护公司(SIPC)的成员。

在新加坡,moomoo上的投资产品和服务是通过Moomoo Financial Singapore Pte. Ltd.提供,该公司受新加坡金融管理局(MAS)监管(牌照号码︰CMS101000) ,持有资本市场服务牌照 (CMS) ,持有财务顾问豁免(Exempt Financial Adviser)资质。本内容未经新加坡金融管理局的审查。

在澳大利亚,moomoo上的金融产品和服务是通过Futu Securities (Australia) Ltd提供,该公司是受澳大利亚证券和投资委员会(ASIC)监管的澳大利亚金融服务许可机构(AFSL No. 224663)。请阅读并理解我们的《金融服务指南》、《条款与条件》、《隐私政策》和其他披露文件,这些文件可在我们的网站 https://www.moomoo.com/au中获取。

在加拿大,通过moomoo应用提供的仅限订单执行的券商服务由Moomoo Financial Canada Inc.提供,并受加拿大投资监管机构(CIRO)监管。

在马来西亚,moomoo上的投资产品和服务是通过Moomoo Securities Malaysia Sdn. Bhd. 提供,该公司受马来西亚证券监督委员会(SC)监管(牌照号码︰eCMSL/A0397/2024) ,持有资本市场服务牌照 (CMSL) 。本内容未经马来西亚证券监督委员会的审查。

Moomoo Technologies Inc., Moomoo Financial Inc., Moomoo Financial Singapore Pte. Ltd., Futu Securities (Australia) Ltd, Moomoo Financial Canada Inc.,和Moomoo Securities Malaysia Sdn. Bhd.是关联公司。

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用浏览器的分享功能,分享给你的好友吧