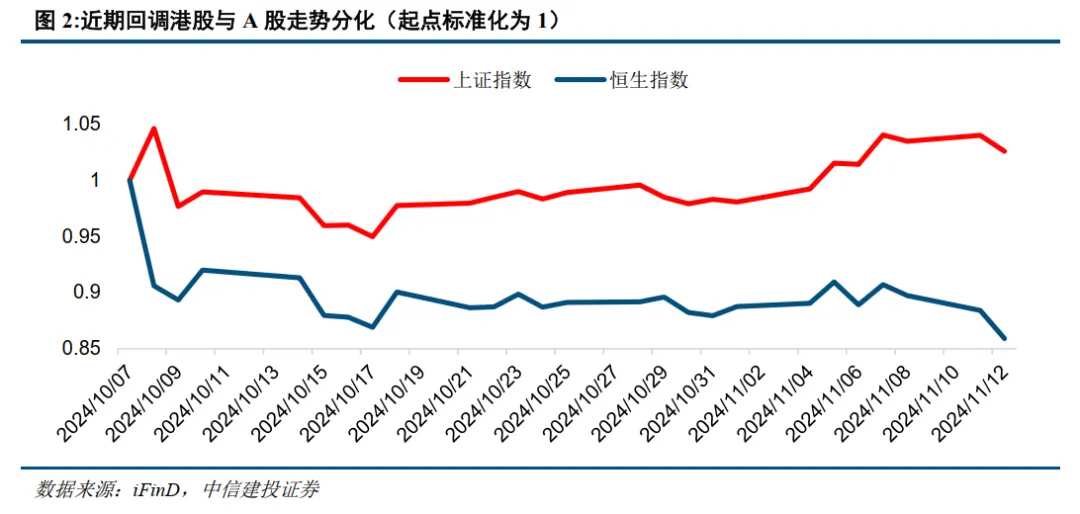

港股在10月8日开启回调,回调时期走势与A股明显分化,AH溢价再度来到高位。这主要是由于港股由机构投资者主导、对主题投资接纳度低,以及港股受特朗普交易短期冲击更显著。当前恒生指数已跌去之前涨幅的2/3以上,我们认为结合本阶段利多与利空因素较平衡的背景看,当前港股回调已较为充分。

港股在10月8日开启回调,回调时期走势与A股明显分化,AH溢价再度来到高位。这主要是由于港股由机构投资者主导、对主题投资接纳度低,以及港股受特朗普交易短期冲击更显著。当前恒生指数已跌去之前涨幅的2/3以上,我们认为结合本阶段利多与利空因素较平衡的背景看,当前港股回调已较为充分。

Source: China Securities Co.,Ltd. Research

Author: Chen Guo, He Sheng

Hong Kong stocks have been continuously correcting since October 8, with the hang seng index dropping more than two-thirds of the gains made from September 25 to October 7. During the correction period, there have been both bullish and bearish factors, so the current decline in Hong Kong stocks should be considered relatively ample. With the recent decline in Hong Kong stocks and the divergence in trends between Hong Kong and A-shares, the valuation of Hong Kong stocks and the AH premium again reflect high cost-effectiveness. Currently, Trump's victory has impacted the trend of Hong Kong stocks, but in the medium term, Trump's policy proposals are favorable for Hong Kong stock liquidity. Therefore, it is believed that following the end of the short-term impact, Hong Kong stocks may welcome a rising market, and this is an extremely cost-effective time to invest in Hong Kong stocks, particularly recommending the technology sector.

Has the current pullback in the Hong Kong stock market been sufficient?

The Hong Kong stock market began its pullback on October 8, showing a significant divergence in the movement during the pullback period compared to the A-shares, with the AH premium back at a high level. This is mainly due to the Hong Kong market being dominated by institutional investors, a low acceptance of thematic investment, and the Hong Kong market being more significantly impacted by the short-term effects of Trump's trading. Currently, the Hang Seng Index has dropped more than 2/3 of its previous gains. We believe that considering the relatively balanced background of bullish and bearish factors at this stage, the current pullback in the Hong Kong stock market has been quite sufficient.

The Hong Kong stock market began its pullback on October 8, showing a significant divergence in the movement during the pullback period compared to the A-shares, with the AH premium back at a high level. This is mainly due to the Hong Kong market being dominated by institutional investors, a low acceptance of thematic investment, and the Hong Kong market being more significantly impacted by the short-term effects of Trump's trading. Currently, the Hang Seng Index has dropped more than 2/3 of its previous gains. We believe that considering the relatively balanced background of bullish and bearish factors at this stage, the current pullback in the Hong Kong stock market has been quite sufficient.

What is the latest position of the large cycle of the Hong Kong stock market?

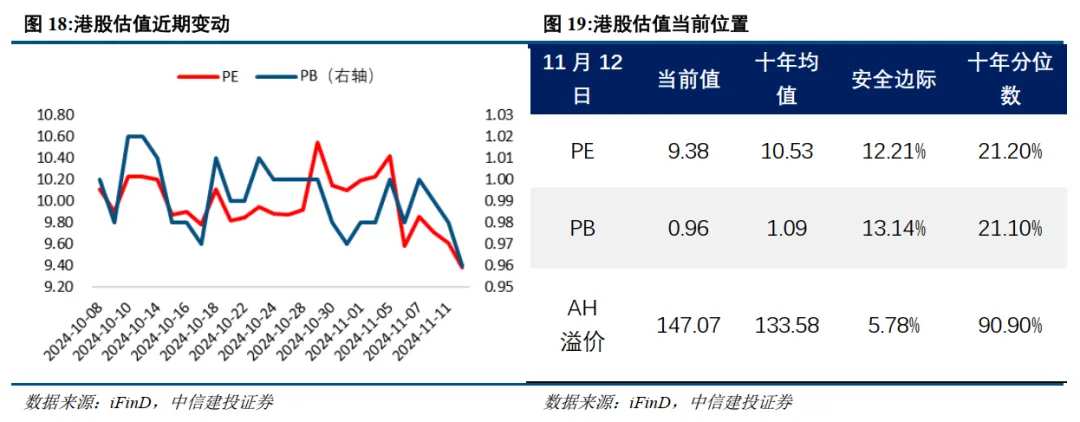

The earnings growth rate recovery of the Hong Kong stock market shows a leading advantage compared to the domestic fundamentals, particularly in the information technology sector and non-essential consumer goods sector. In terms of valuation, after the recent pullback, the PE and PB percentile over the past ten years have decreased to the 21.2% and 21.1% percentiles respectively, while the AH premium has risen and the dividend yield still has a high margin of safety.

How to view the subsequent trend of the Hong Kong stock market in the context of Trump's presidency?

Trump's tax reduction proposals and his tendency to pressure the Federal Reserve for interest rate cuts are beneficial to the total overseas liquidity, while his trade restrictions against China are not favorable for the allocation ratio of overseas liquidity to Hong Kong stocks. Since Trump tends to prioritize domestic economic policies, after the recent short-term shock subsides, liquidity is expected to flow back to Hong Kong stocks, making the current layout of Hong Kong stocks highly cost-effective. Among the various sectors of Hong Kong stocks, the technology internet sector shows a significant recovery in profits, benefits from a wave of dividends and stock repurchase in valuation, and enjoys the favor of foreign capital in liquidity, making it the most worthy of attention.

1. Introduction

After a strong rise from September 25 to October 7, Hong Kong stocks began to sharply adjust from October 8. During the rapid increase from September 25 to October 7, the hang seng index accumulated a rise of 20.8%, and the hang seng tech index accumulated a rise of 37.3%. As of November 12, the hang seng tech index has dropped 17.3% since its peak on October 7, while the hang seng index has fallen by 14.1%, having lost 46% and 68% of their previous gains respectively.

The large cycle of Hong Kong stocks shows a structural upward trend, with valuation positions providing cost-effectiveness. After the sharp rise in early October, the valuation cycle position of Hong Kong stocks has slightly deviated, and as Hong Kong stocks have recently experienced a significant correction, this article will address the following questions: Is the current correction in Hong Kong stocks sufficient? What is the latest position of the large cycle of Hong Kong stocks? How to view the subsequent trends of Hong Kong stocks under the background of Trump taking office?

Second, is the current correction in Hong Kong stocks sufficient?

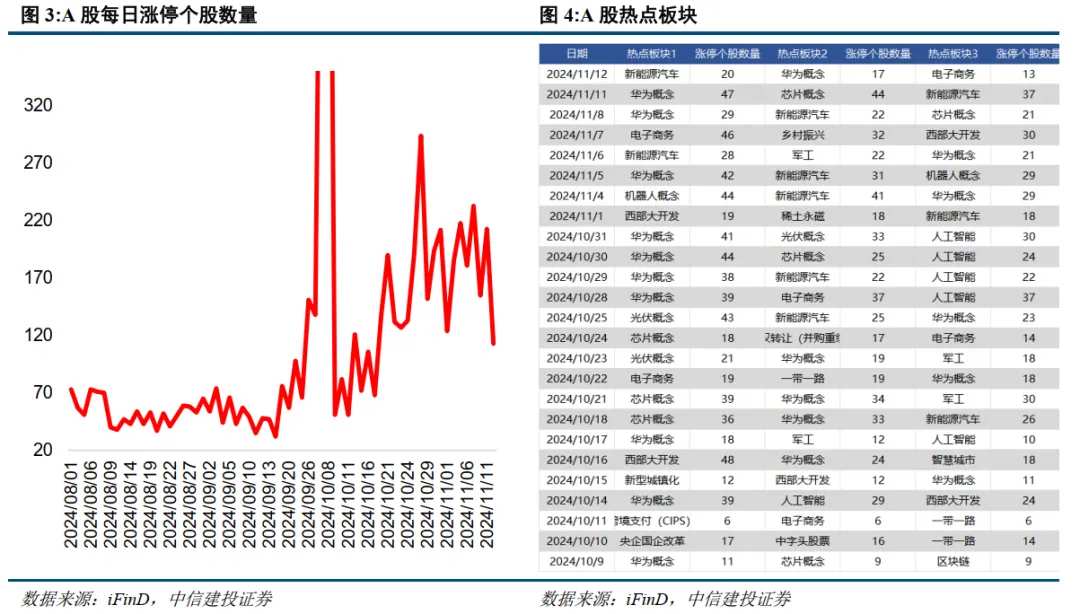

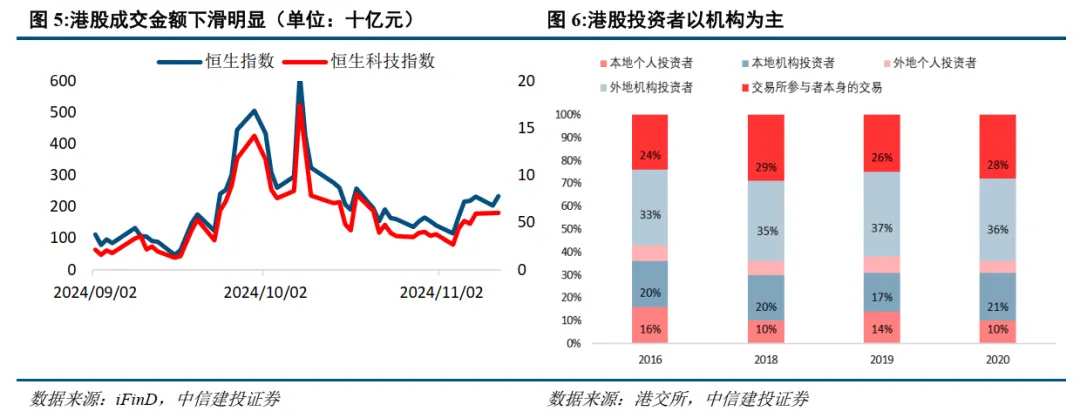

Recently, there has been a significant divergence between the movements of Hong Kong and A shares during the correction, which is related to the different acceptance of thematic investment by the two markets. Since the peak correction on October 8, A shares have remained robust, with another rise recently. The recent market activity in A shares is mainly supported by structural trends, maintaining high enthusiasm for themes such as self-control, with many stocks also being sought after. Since October 9, the average daily number of stocks reaching their daily limit in the A-share market has been 150, significantly higher than before September 25. Compared to the popularity of thematic investment in A shares, Hong Kong stocks have a lower acceptance of thematic investments. Among the various investors in Hong Kong stocks, foreign institutional investors have long accounted for over 35% in recent years, while local institutional investors have maintained around 20%. Therefore, excluding the trading by exchange participants themselves, Hong Kong stocks are clearly dominated by institutional investors. The structure of investors in Hong Kong stocks, mainly consisting of institutions, has led to a significant decline in trading enthusiasm after the overall market situation retreated, with the transaction amount of the hang seng tech index declining by at most 84.7% since the peak on October 8, while the transaction amount of the hang seng index has fallen by at most 81.3%.

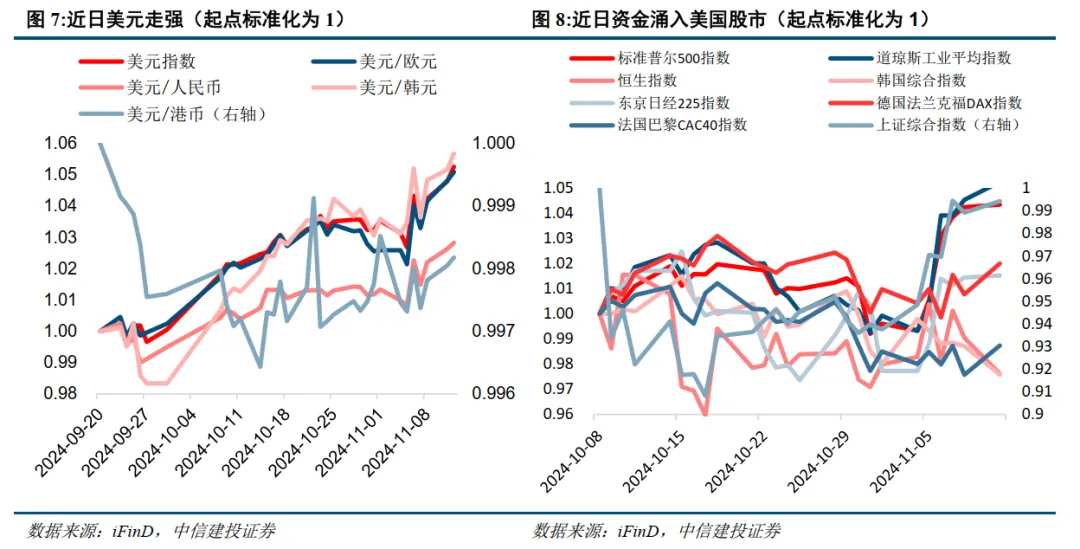

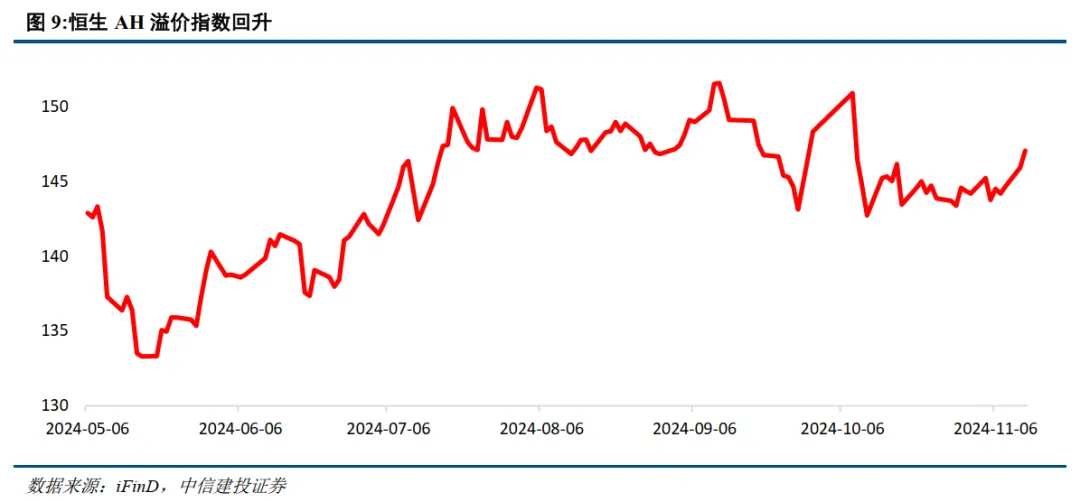

Trump's trades have resulted in capital outflow from global markets, significantly impacting Hong Kong stocks and exacerbating the divergence between Hong Kong and A shares, with a substantial rebound in AH premiums. Trump's trades surged before and after his election. Overseas funds have flowed from the Asia-Pacific and European markets to the USA, with the dollar sharply appreciating against other currencies, and the US stock market rising strongly, while other major stock markets have performed relatively poorly. As an offshore market, Hong Kong stocks are significantly influenced by overseas liquidity, with Trump's trades leading to significant outflows from the Hong Kong stock market. Additionally, they are also affected by Sino-US relations, as the expectations of deteriorating Sino-US relations after Trump took office have led to a reduction in the liquidity allocation to Hong Kong stocks by foreign capital. Consequently, multiple factors leading to different trends between A shares and Hong Kong stocks during the recent correction have caused the AH premium to rise again. As of November 12, the hang seng AH stock premium index has risen to 47%, placing it at the 90.9% percentile over the past decade.

The current adjustment of Hong Kong stocks has been quite sufficient. Since the correction on October 8, the hang seng index and the hang seng tech index have dropped 68% and 46% of their increases from September 25 to October 7, respectively. During this round of correction, both bullish and bearish factors have existed: the comprehensive policies introduced on September 24 have continued to have an impact, the debt reduction policies launched on November 8 have again generated policy benefits, while Trump's trades have had negative effects on the liquidity of Hong Kong stocks. However, expectations surrounding Trump's accession to power actually existed before September 25, and from July to September, Trump's media technology stocks remained at a high position, thus its pricing role during this round of Hong Kong stock correction should have weakened. In the context of a relative balance between bullish and bearish factors, the recent decline in Hong Kong stocks has indeed been quite sufficient.

Three, where is the latest position of the Hong Kong stock big cycle?

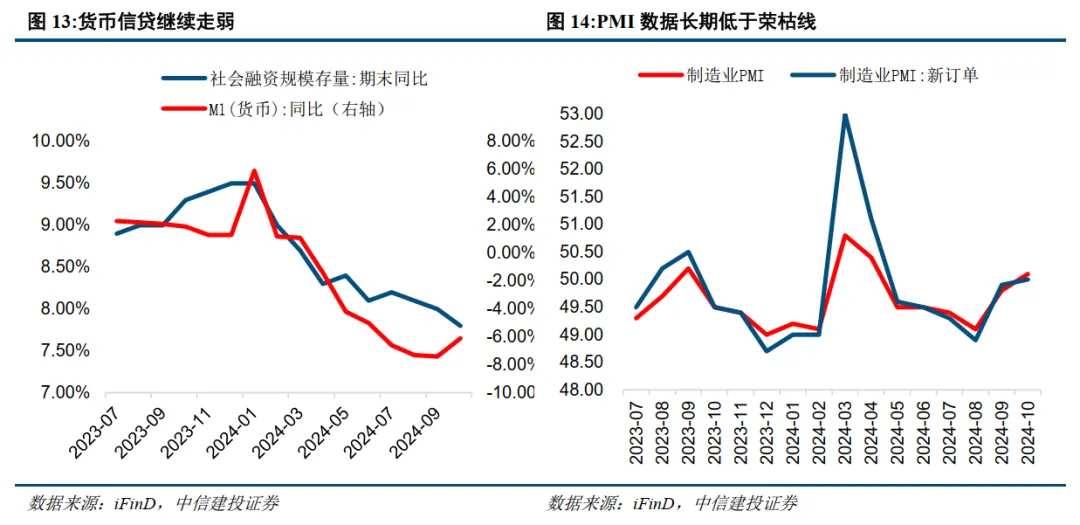

The overall profit cycle of Hong Kong stocks is greatly influenced by domestic fundamentals, but the current recovery progress shows a leading advantage. In the latest reporting period, the profit growth rate of the hang seng index was 6.43%, rising for four consecutive reporting periods, with the previous profit growth rate at -2.09%; the latest revenue growth rate was -0.11%, slightly better than the previous period. From the data, the overall profitability of Hong Kong stocks has begun to recover. In the report "Where is the Hong Kong Stock Big Cycle?" it is pointed out that the cycle fluctuations of Hong Kong stocks are generally consistent with the cycle fluctuations of domestic economic fundamentals, and the current profit growth of Hong Kong stocks is still dragged down by domestic fundamentals. However, compared to the continuous weakening of monetary credit data such as domestic M1 and social financing year-on-year growth rates, and the continuing weak fundamentals, the profitability of Hong Kong companies has started to recover, reflecting the advantage in the profit cycle.

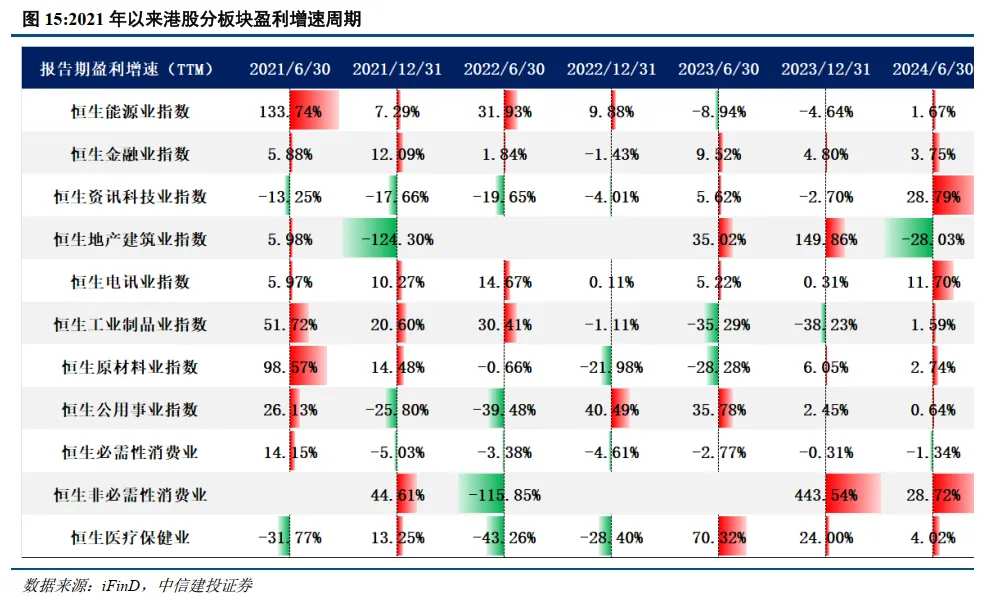

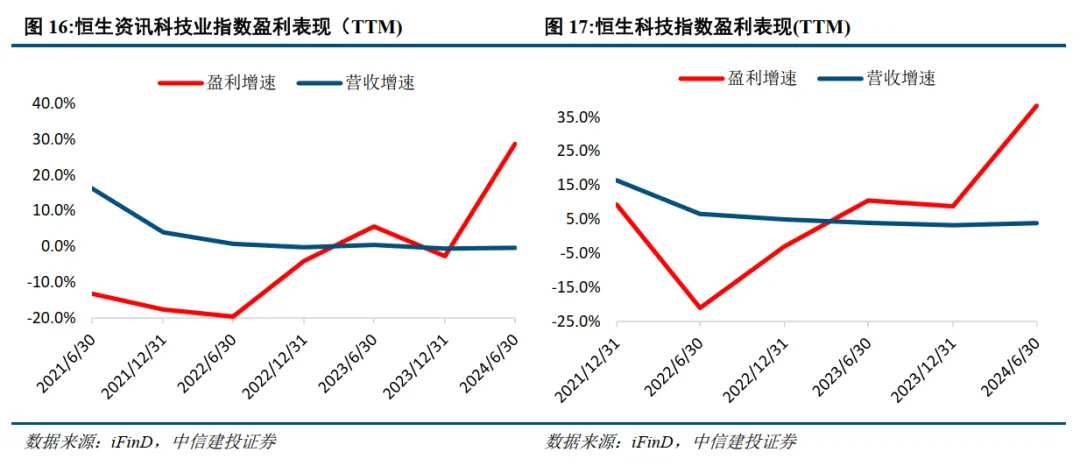

During the recovery of Hong Kong stocks, the information technology industry and the non-essential consumption sector performed remarkably. In the latest reporting period, the profit growth rate of the hang seng information technology industry index and the hang seng non-essential consumption industry far outpaced other sectors, at 28.79% and 28.72% respectively. Similarly, the hang seng tech index, which represents Hong Kong's technology internet stocks, performed even better in profit growth compared to the hang seng information technology industry index. As of the first half of this year, the profit growth rate of the hang seng tech index has risen consecutively for several reporting periods, showing significant recovery, with the latest profit growth rate reaching 38.32%. Compared to profit growth rates, the revenue growth rates of the hang seng information technology industry index and the hang seng tech index were both weaker, with the latest reporting period data at -0.38% and 3.91% respectively. This difference hints that the logic of the current profit recovery of Hong Kong network technology stocks is not an expansive recovery but is related to the business structure adjustment and improvement of operational efficiency of various network technology companies. The profit growth rate recovery of the hang seng non-essential consumption sector is relatively synchronized with revenue growth rate recovery, forming a significant rebound in the second half of 2023, with continued positive growth in the first half of 2024, primarily benefiting from the ongoing post-epidemic recovery.

The valuation of Hong Kong stocks has returned to a high cost-performance position after recent adjustments. As of November 12, the PE of the hang seng index has decreased to 9.38, and the PB has dropped to 0.96, while the decile ranks based on the ten-year average have decreased from over 40% and 30% in October to 21.2% and 21.1%, respectively, with safety margins calculated based on the ten-year averages at 12.21% and 13.14%. Currently, the AH premium is at 47.07%, and the safety margin is at 5.78%, placing it at the 90.9% decile of the last ten years. Therefore, the valuations of Hong Kong stocks based on the PE method, PB method, and AH premium method all show sufficient upward potential. In terms of the safety margin provided by the high dividend yield of Hong Kong stocks, as of November 11, the AH stocks in the hang seng high dividend yield index have retained a large safety margin. Among them, the safety margins of cnooc, china construction bank corporation, and china citic bank corporation in terms of dividend yield are the highest, at 94.81%, 61.38%, and 58.77% respectively, so the safety margins of high dividend yield stocks in Hong Kong stocks are also quite sufficient, and the dividend in Hong Kong stocks still has cost-performance advantages.

The liquidity cycle has entered a favorable position, but caution is needed as concerns about a possible recession in the usa may lead to outflows from the Asia-Pacific stock markets. Looking back at the performance of the Asia-Pacific markets under the changes in the Federal Reserve's monetary policy over the past thirty years, it is found that in the past four rounds of easing cycles, the initiation of two of those cycles did not bring any increase in liquidity to the Asia-Pacific stock markets: In January 2001, in response to the prolonged economic downturn following the burst of the internet bubble, the Federal Reserve initiated an interest rate cut cycle, but with high recession concerns, the Asia-Pacific stock markets declined, and the high volatility of the usd index also reflected that funds did not flow out; in September 2007, during the outbreak of the global financial crisis, the Federal Reserve made an emergency rate cut, and in the early days of this rate cut, the Asia-Pacific stock markets significantly declined, while the usd index entered an upward cycle after a brief decline. Both of these cycles were rooted in concerns over a recession or the risk of recession in the usa. In fact, due to the Asia-Pacific region's focus on manufacturing, overall economic fluctuations are greater, so in addition to the extent of the Federal Reserve's monetary easing, the liquidity of Asia-Pacific stock markets also relies on foreign capital's risk appetite. Currently entering the latest round of interest rate cuts, the overall liquidity overseas has improved, but attention still needs to be paid to the slowdown in the usa job market.

Four, how to view the subsequent trends of Hong Kong stocks under the backdrop of Trump taking office?

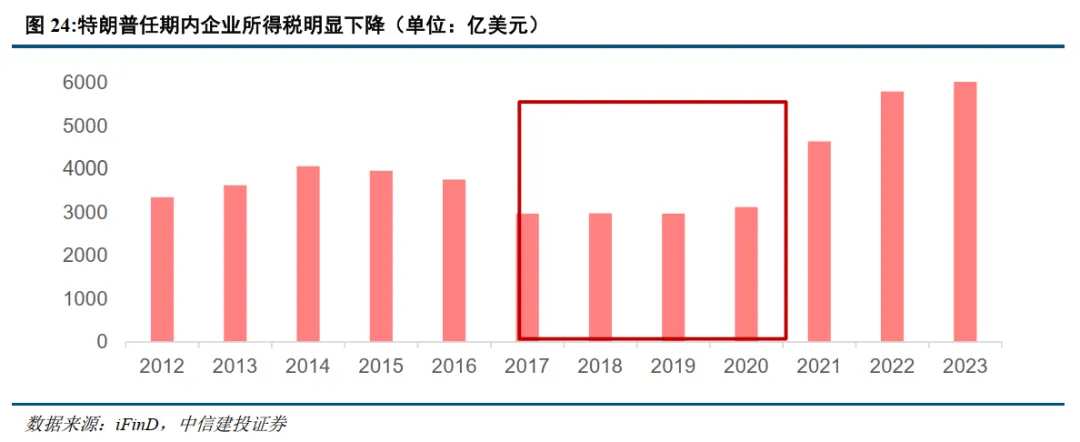

Trump’s taking office overall benefits overseas liquidity; after a short-term impact, Hong Kong stocks may regain upward momentum, and now is a favorable time for layout. The liquidity of Hong Kong stocks is influenced by the total amount of overseas liquidity on one hand, and on the other hand, by the distribution proportion of overseas liquidity. The total overseas liquidity benefits from Trump's assumption of office. During his previous term, Trump passed the fourth-largest tax reduction plan in history, significantly lowering corporate income taxes during his term, and in this round, Trump will continue to advocate tax cuts. Large-scale tax cuts will lead to reduced fiscal revenue and government spending cuts, thereby exerting pressure on economic growth in the usa in the short term while stimulating interest rate cuts. Additionally, Trump has repeatedly commented publicly on the Federal Reserve's monetary policy decisions and has promised the public a goal of "low interest rates," which is conducive to increasing the intensity of interest rate cuts. The distribution proportion of overseas liquidity is negatively affected by Trump's taking office, as concerns over deteriorating sino-us relations may lead to a smaller distribution of liquidity to Hong Kong stocks due to risk aversion. However, overall, the concerns triggered by Trump's taking office in the short term have generally been reflected in pricing. In the medium to long-term, Trump gives domestic monetary and fiscal policies a higher priority, so overseas liquidity is still benefited by Trump taking office, and after recent shocks, foreign capital may flow back into Hong Kong stocks. The favorable conditions of improved liquidity combined with the valuation correction and early profit recovery make now an appropriate time to position in Hong Kong stocks.

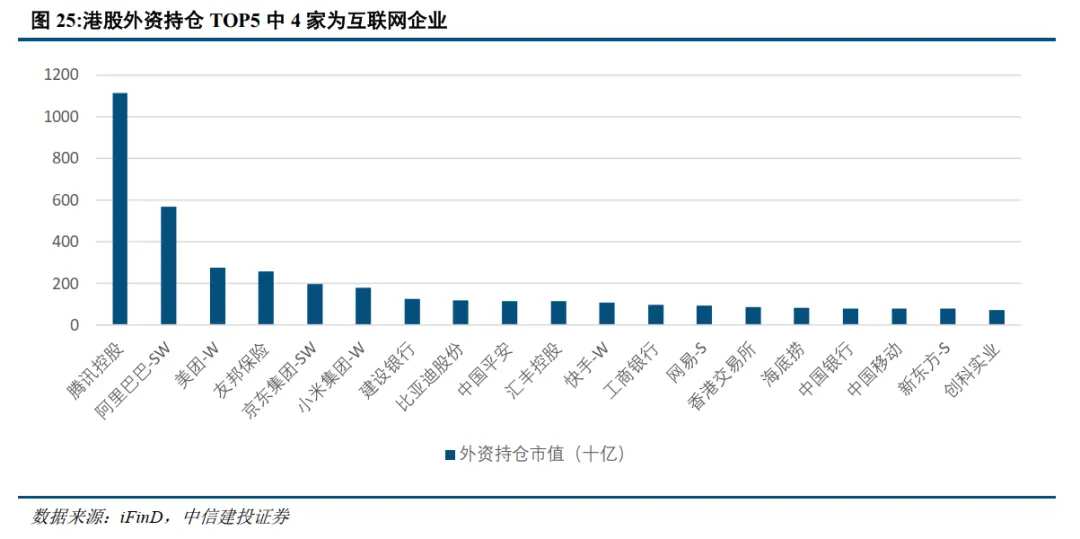

Priority recommendation for the Hong Kong stock sector is technology internet, with high cost-performance in the dividend sector. Currently, all three major cycles of the network technology sector are in favorable positions. In the profit cycle, the profit growth rate of the network technology sector has continuously and significantly recovered, showing clear signs of prosperity; in the liquidity cycle, the Federal Reserve has entered a rate cut cycle, and Trump's victory is expected to enhance the intensity of interest rate cuts, with Hong Kong internet, as a favored sector of foreign capital, benefiting first from improvements in overseas liquidity; in terms of valuation, leading stocks in Hong Kong's network technology are shifting towards a business model that emphasizes returns to investors, initiating a wave of dividend buybacks to boost valuations. Therefore, leading stocks in Hong Kong's network technology deserve special attention. Regarding dividends in Hong Kong stocks, PE, PB, and AH premium have provided sufficient safety margins after recent adjustments, and their combination with the high dividend yield safety margins once again brings the cost-performance of Hong Kong stock dividends to a high level.

Risk warning

(1) Geopolitical risks. If the management of geopolitical relations is not well handled, it could affect foreign investment preferences for Hong Kong stocks. At the same time, hotspots such as the Russia-Ukraine conflict and Middle East issues may face risks of deterioration, which could negatively impact the market if a crisis occurs.

(2) If the US economy continues to maintain its resilience and economic data such as labor market and retail perform well, then the risk of a US recession may be reassessed. At the same time, inflation risks will also face rebounds, and the Fed's tightness against inflation will continue, and global liquidity may be looser than expected, putting pressure on Hong Kong stock liquidity.

(3) The effect of domestic economic recovery or steady growth policies may fall short of expectations. If subsequent domestic real estate sales, investments, and other data take a long time to recover, the long-standing debt repayment risks of city investment will resurface, and if economic recovery is not as expected, the overall market trend will be under pressure, with overly optimistic pricing expectations facing correction.

Editor/rice