GCShutter

J.P. Morgan expects demand uncertainty to prevail in the IT and BPO sector in 2023, counterbalanced by improving supply.

The reset in demand trajectory that some companies highlighted in H2 is expected to become more prevalent in the coming half, with buyers possibly continuing to delay new project awards and prioritize projects that generate quick ROI or cut costs.

However, demand trends could improve in H2 2023, driven by pent up spending.

The IT/BPO stocks were down 37% YTD, compared to the S&P 500 index that was down by mere 15%, the company said in a research report.

The company has cut its H1 growth estimates for most IT/BPO companies, bringing the estimates lower than the Wallstreet consensus for most names.

J.P. Morgan sees Wallstreet revenue estimates for 2023 as too high.

The company upgraded DXC Technology (DXC) to Neutral from Underweight, considering a more defensive revenue mix and margin expansion in 2023.

Meanwhile, Cognizant Technology Solutions (CTSH) was downgraded to Underweight from Neutral on the weak macro environment.

Genpact (G), TELUS International (TIXT) and CI&T (CINT) were downgraded to Neutral from Overweight. WNS (WNS) is preferred over G, TaskUs (TASK) over TIXT and Grid Dynamics Holdings (GDYN) or Thoughtworks Holding (TWKS) over CINT.

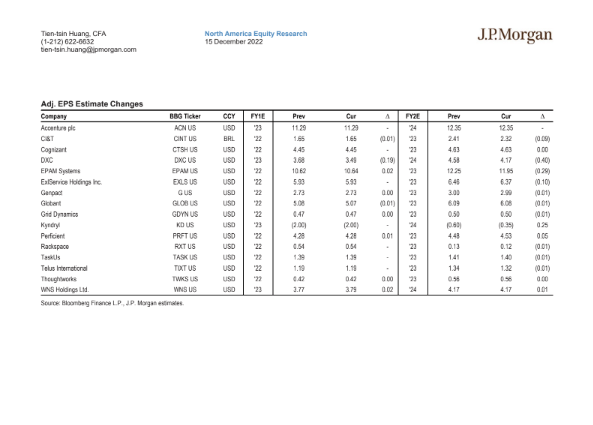

Here is a look at the adjusted EPS estimate changes for the IT/BPO companies: