Generally speaking long term investing is the way to go. But unfortunately, some companies simply don't succeed. To wit, the The Bank of East Asia, Limited (HKG:23) share price managed to fall 72% over five long years. That's not a lot of fun for true believers. The falls have accelerated recently, with the share price down 13% in the last three months. However, one could argue that the price has been influenced by the general market, which is down 19% in the same timeframe.

Since Bank of East Asia has shed HK$833m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

View our latest analysis for Bank of East Asia

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

While the share price declined over five years, Bank of East Asia actually managed to increase EPS by an average of 1.5% per year. So it doesn't seem like EPS is a great guide to understanding how the market is valuing the stock. Or possibly, the market was previously very optimistic, so the stock has disappointed, despite improving EPS.

By glancing at these numbers, we'd posit that the the market had expectations of much higher growth, five years ago. Having said that, we might get a better idea of what's going on with the stock by looking at other metrics.

The steady dividend doesn't really explain why the share price is down. It's not immediately clear to us why the stock price is down but further research might provide some answers.

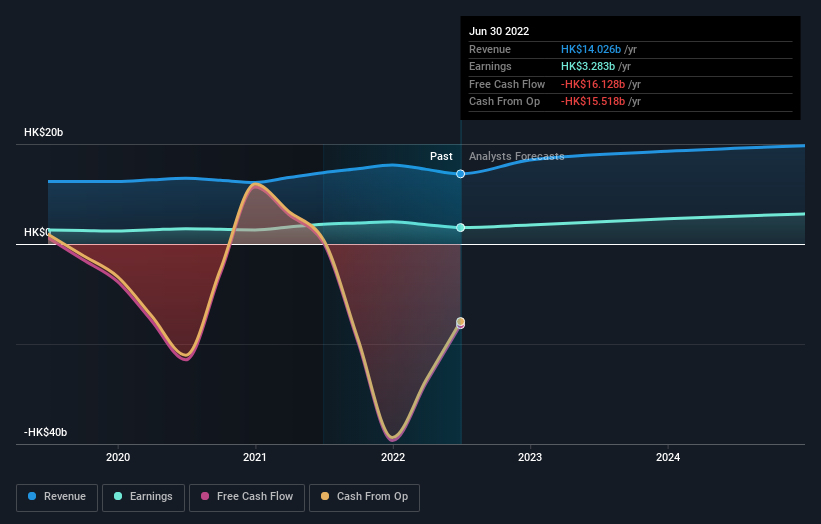

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

SEHK:23 Earnings and Revenue Growth September 28th 2022

SEHK:23 Earnings and Revenue Growth September 28th 2022If you are thinking of buying or selling Bank of East Asia stock, you should check out this FREE detailed report on its balance sheet.

What About Dividends?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. It's fair to say that the TSR gives a more complete picture for stocks that pay a dividend. As it happens, Bank of East Asia's TSR for the last 5 years was -66%, which exceeds the share price return mentioned earlier. And there's no prize for guessing that the dividend payments largely explain the divergence!

A Different Perspective

While it's certainly disappointing to see that Bank of East Asia shares lost 19% throughout the year, that wasn't as bad as the market loss of 22%. What is more upsetting is the 11% per annum loss investors have suffered over the last half decade. While the losses are slowing we doubt many shareholders are happy with the stock. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 1 warning sign with Bank of East Asia , and understanding them should be part of your investment process.

Of course Bank of East Asia may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on HK exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.