Jiangsu Sunshine Co., Ltd. (SHSE:600220) shares have had a horrible month, losing 27% after a relatively good period beforehand. Looking back over the past twelve months the stock has been a solid performer regardless, with a gain of 11%.

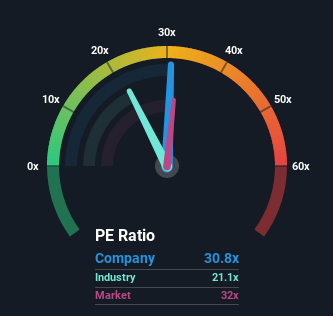

Although its price has dipped substantially, you could still be forgiven for feeling indifferent about Jiangsu Sunshine's P/E ratio of 30.8x, since the median price-to-earnings (or "P/E") ratio in China is also close to 32x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Recent times have been quite advantageous for Jiangsu Sunshine as its earnings have been rising very briskly. The P/E is probably moderate because investors think this strong earnings growth might not be enough to outperform the broader market in the near future. If that doesn't eventuate, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

See our latest analysis for Jiangsu Sunshine

SHSE:600220 Price Based on Past Earnings September 19th 2022 Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Jiangsu Sunshine will help you shine a light on its historical performance.

SHSE:600220 Price Based on Past Earnings September 19th 2022 Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Jiangsu Sunshine will help you shine a light on its historical performance. Is There Some Growth For Jiangsu Sunshine?

Jiangsu Sunshine's P/E ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the market.

If we review the last year of earnings growth, the company posted a terrific increase of 198%. As a result, it also grew EPS by 19% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 41% shows it's noticeably less attractive on an annualised basis.

With this information, we find it interesting that Jiangsu Sunshine is trading at a fairly similar P/E to the market. It seems most investors are ignoring the fairly limited recent growth rates and are willing to pay up for exposure to the stock. They may be setting themselves up for future disappointment if the P/E falls to levels more in line with recent growth rates.

The Key Takeaway

With its share price falling into a hole, the P/E for Jiangsu Sunshine looks quite average now. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Jiangsu Sunshine revealed its three-year earnings trends aren't impacting its P/E as much as we would have predicted, given they look worse than current market expectations. Right now we are uncomfortable with the P/E as this earnings performance isn't likely to support a more positive sentiment for long. If recent medium-term earnings trends continue, it will place shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 5 warning signs with Jiangsu Sunshine (at least 2 which don't sit too well with us), and understanding these should be part of your investment process.

You might be able to find a better investment than Jiangsu Sunshine. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a P/E below 20x (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.