Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that United Company RUSAL, International Public Joint-Stock Company (HKG:486) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for United Company RUSAL International

What Is United Company RUSAL International's Net Debt?

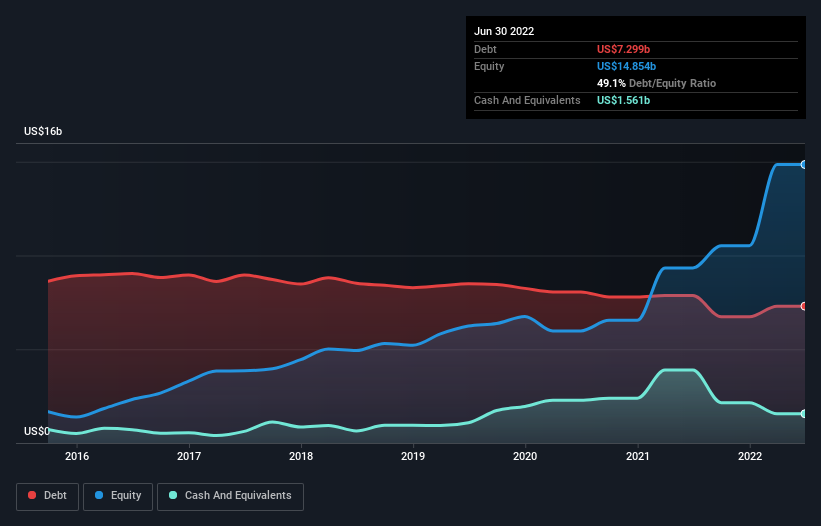

As you can see below, United Company RUSAL International had US$7.30b of debt at June 2022, down from US$7.87b a year prior. On the flip side, it has US$1.56b in cash leading to net debt of about US$5.74b.

SEHK:486 Debt to Equity History September 15th 2022

SEHK:486 Debt to Equity History September 15th 2022A Look At United Company RUSAL International's Liabilities

According to the last reported balance sheet, United Company RUSAL International had liabilities of US$5.85b due within 12 months, and liabilities of US$4.72b due beyond 12 months. On the other hand, it had cash of US$1.56b and US$2.08b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$6.93b.

This deficit is considerable relative to its market capitalization of US$8.03b, so it does suggest shareholders should keep an eye on United Company RUSAL International's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

United Company RUSAL International's net debt to EBITDA ratio of about 1.7 suggests only moderate use of debt. And its strong interest cover of 10.2 times, makes us even more comfortable. Notably, United Company RUSAL International's EBIT launched higher than Elon Musk, gaining a whopping 111% on last year. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if United Company RUSAL International can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, United Company RUSAL International saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

United Company RUSAL International's conversion of EBIT to free cash flow and level of total liabilities definitely weigh on it, in our esteem. But the good news is it seems to be able to grow its EBIT with ease. Looking at all the angles mentioned above, it does seem to us that United Company RUSAL International is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 3 warning signs we've spotted with United Company RUSAL International (including 2 which make us uncomfortable) .

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.