Just because a business does not make any money, does not mean that the stock will go down. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So, the natural question for Revolution Medicines (NASDAQ:RVMD) shareholders is whether they should be concerned by its rate of cash burn. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

Check out our latest analysis for Revolution Medicines

Does Revolution Medicines Have A Long Cash Runway?

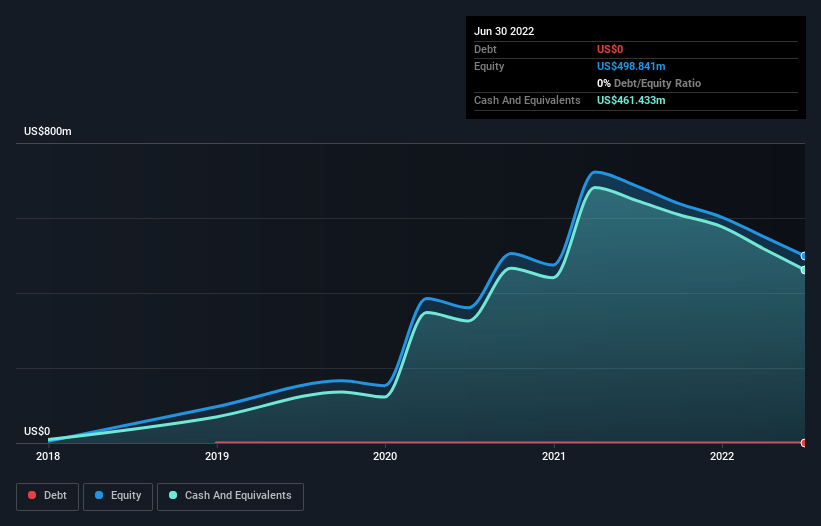

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at June 2022, Revolution Medicines had cash of US$461m and no debt. In the last year, its cash burn was US$193m. So it had a cash runway of about 2.4 years from June 2022. Arguably, that's a prudent and sensible length of runway to have. The image below shows how its cash balance has been changing over the last few years.

NasdaqGS:RVMD Debt to Equity History September 15th 2022

NasdaqGS:RVMD Debt to Equity History September 15th 2022How Well Is Revolution Medicines Growing?

At first glance it's a bit worrying to see that Revolution Medicines actually boosted its cash burn by 48%, year on year. And we must say we find it concerning that operating revenue dropped 32% over the same period. Considering both these metrics, we're a little concerned about how the company is developing. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Hard Would It Be For Revolution Medicines To Raise More Cash For Growth?

Revolution Medicines seems to be in a fairly good position, in terms of cash burn, but we still think it's worthwhile considering how easily it could raise more money if it wanted to. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Revolution Medicines' cash burn of US$193m is about 11% of its US$1.7b market capitalisation. Given that situation, it's fair to say the company wouldn't have much trouble raising more cash for growth, but shareholders would be somewhat diluted.

So, Should We Worry About Revolution Medicines' Cash Burn?

On this analysis of Revolution Medicines' cash burn, we think its cash runway was reassuring, while its falling revenue has us a bit worried. While we're the kind of investors who are always a bit concerned about the risks involved with cash burning companies, the metrics we have discussed in this article leave us relatively comfortable about Revolution Medicines' situation. Separately, we looked at different risks affecting the company and spotted 4 warning signs for Revolution Medicines (of which 1 is a bit unpleasant!) you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.