jpbcpa/iStock via Getty Images

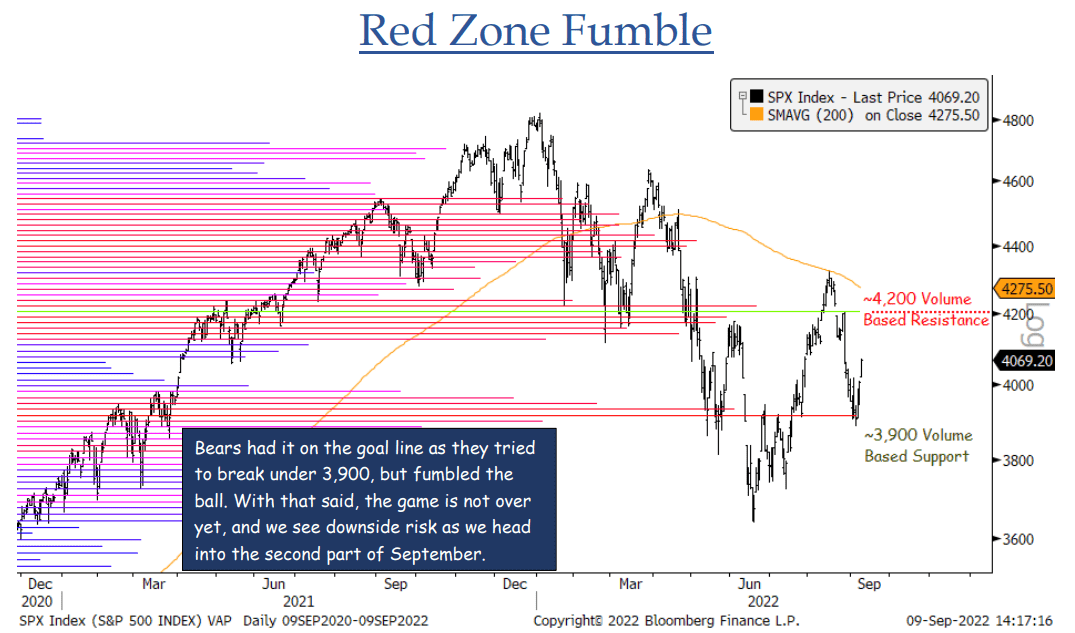

Equity sellers failed to push the S&P 500 (SP500) (NYSEARCA:SPY) below the technically important 3,900 level last week, but it isn't clear sailing for more market gains, according to Jonathan Krinksy, chief market technician at BTIG.

"Bears fumbled on the goal line as they tried to break under 3,900 last week, but the game is not over yet," Krinsky wrote in his latest note. "We see downside risk as we head into the seasonally weak second part of September."

"While the dollar (USDOLLAR) (UUP) and rates paused their ascent, there was no reversal and 10yr (US10Y) (TBT) (TLT) real rates actually closed at fresh 52wk highs," he said. "The SPX put in a bullish engulfing week which can carry some upside into next week, but ultimately we don't see it running away to the upside here."

"Seasonality is just one part of the puzzle, and never to be relied upon by itself," he added. "With that said, on average the back half of September is typically one of the most difficult periods for the market."

More than 50% of Russell 3000 (IWV) stocks rising above their 50-day moving averages would help confirm a "more durable uptrend" in stocks, according to Krinsky. That measure peaked at 47% in August.

"DXY needs below 107 to break trend, 105 to reverse it," he said. "10yr yields need to break under 3.20%. Real rates also suggest the bounce in Nasdaq (COMP.IND) (QQQ) a bit too optimistic."

Energy stocks (XLE) remain in a firm uptrend, even with crude oil (CL1:COM) (USO) breaking below $82 per barrel, Krinsky noted.

"We tend to go with the equities over the commodity and therefore would stick with some exposure here. Uranium (URNM) still a constructive base."

Is the stock market facing Goldilocks' evil twin?