Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Jiangsu Lopal Tech. Co., Ltd. (SHSE:603906) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Jiangsu Lopal Tech

What Is Jiangsu Lopal Tech's Net Debt?

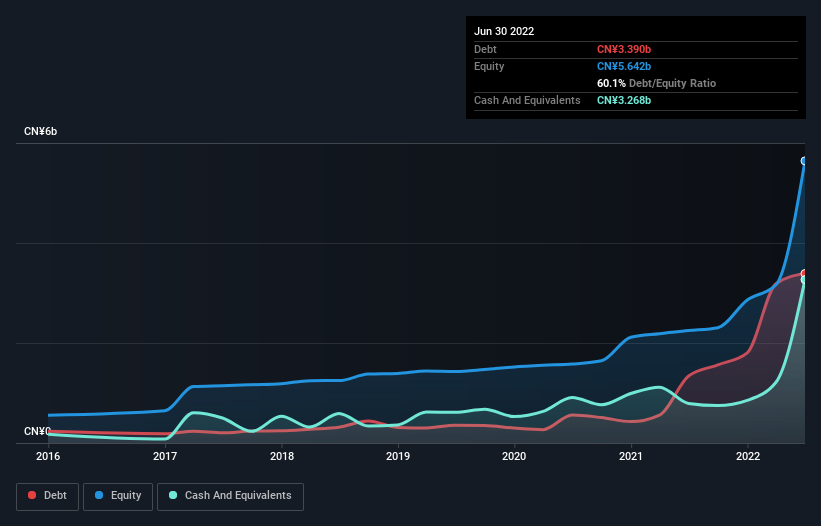

The image below, which you can click on for greater detail, shows that at June 2022 Jiangsu Lopal Tech had debt of CN¥3.39b, up from CN¥1.34b in one year. However, because it has a cash reserve of CN¥3.27b, its net debt is less, at about CN¥122.1m.

SHSE:603906 Debt to Equity History September 7th 2022

SHSE:603906 Debt to Equity History September 7th 2022How Healthy Is Jiangsu Lopal Tech's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Jiangsu Lopal Tech had liabilities of CN¥4.81b due within 12 months and liabilities of CN¥1.19b due beyond that. Offsetting this, it had CN¥3.27b in cash and CN¥2.25b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥486.9m.

Since publicly traded Jiangsu Lopal Tech shares are worth a total of CN¥18.9b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Carrying virtually no net debt, Jiangsu Lopal Tech has a very light debt load indeed.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Jiangsu Lopal Tech has very little debt (net of cash), and boasts a debt to EBITDA ratio of 0.096 and EBIT of 11.3 times the interest expense. Indeed relative to its earnings its debt load seems light as a feather. Better yet, Jiangsu Lopal Tech grew its EBIT by 251% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Jiangsu Lopal Tech can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Jiangsu Lopal Tech burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Jiangsu Lopal Tech's EBIT growth rate suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. But the stark truth is that we are concerned by its conversion of EBIT to free cash flow. Taking all this data into account, it seems to us that Jiangsu Lopal Tech takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 4 warning signs for Jiangsu Lopal Tech (1 is a bit unpleasant!) that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.