Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies JSTI Group (SZSE:300284) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for JSTI Group

What Is JSTI Group's Net Debt?

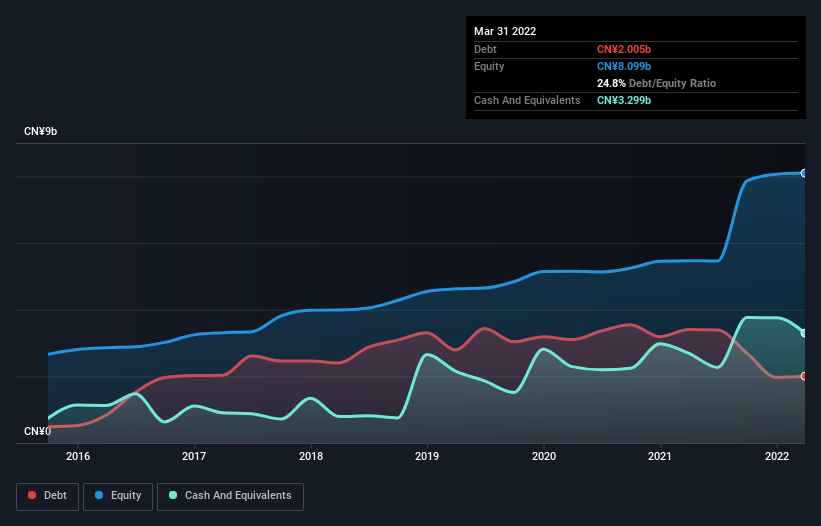

As you can see below, JSTI Group had CN¥2.01b of debt at March 2022, down from CN¥3.40b a year prior. But on the other hand it also has CN¥3.30b in cash, leading to a CN¥1.29b net cash position.

SZSE:300284 Debt to Equity History August 3rd 2022

SZSE:300284 Debt to Equity History August 3rd 2022How Strong Is JSTI Group's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that JSTI Group had liabilities of CN¥5.62b due within 12 months and liabilities of CN¥858.7m due beyond that. Offsetting this, it had CN¥3.30b in cash and CN¥7.75b in receivables that were due within 12 months. So it actually has CN¥4.57b more liquid assets than total liabilities.

This surplus liquidity suggests that JSTI Group's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Succinctly put, JSTI Group boasts net cash, so it's fair to say it does not have a heavy debt load!

But the other side of the story is that JSTI Group saw its EBIT decline by 5.1% over the last year. That sort of decline, if sustained, will obviously make debt harder to handle. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine JSTI Group's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While JSTI Group has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Looking at the most recent three years, JSTI Group recorded free cash flow of 48% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that JSTI Group has net cash of CN¥1.29b, as well as more liquid assets than liabilities. So we don't think JSTI Group's use of debt is risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example - JSTI Group has 2 warning signs we think you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.