Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that NetEase, Inc. (NASDAQ:NTES) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for NetEase

How Much Debt Does NetEase Carry?

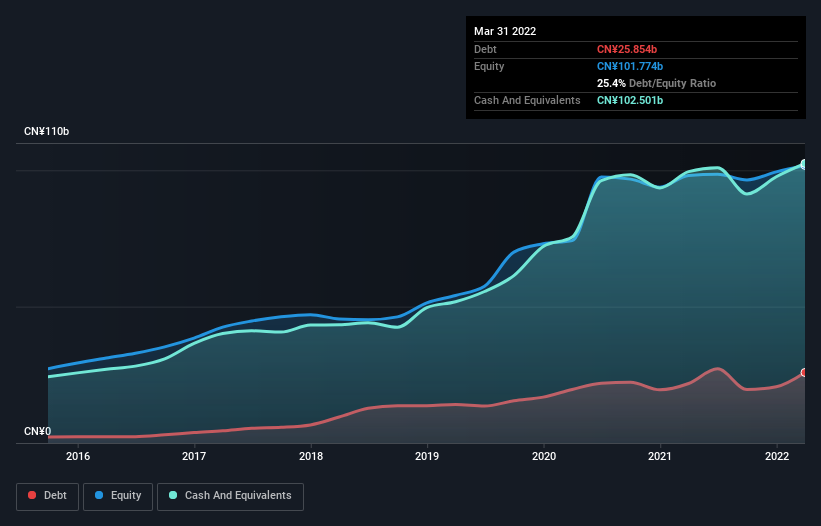

You can click the graphic below for the historical numbers, but it shows that as of March 2022 NetEase had CN¥25.9b of debt, an increase on CN¥21.8b, over one year. However, its balance sheet shows it holds CN¥102.5b in cash, so it actually has CN¥76.6b net cash.

NasdaqGS:NTES Debt to Equity History August 2nd 2022

NasdaqGS:NTES Debt to Equity History August 2nd 2022A Look At NetEase's Liabilities

According to the last reported balance sheet, NetEase had liabilities of CN¥51.8b due within 12 months, and liabilities of CN¥5.71b due beyond 12 months. Offsetting these obligations, it had cash of CN¥102.5b as well as receivables valued at CN¥5.28b due within 12 months. So it can boast CN¥50.3b more liquid assets than total liabilities.

This surplus suggests that NetEase has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that NetEase has more cash than debt is arguably a good indication that it can manage its debt safely.

Another good sign is that NetEase has been able to increase its EBIT by 23% in twelve months, making it easier to pay down debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if NetEase can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. NetEase may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, NetEase actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that NetEase has net cash of CN¥76.6b, as well as more liquid assets than liabilities. And it impressed us with free cash flow of CN¥21b, being 127% of its EBIT. So is NetEase's debt a risk? It doesn't seem so to us. Over time, share prices tend to follow earnings per share, so if you're interested in NetEase, you may well want to click here to check an interactive graph of its earnings per share history.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.