If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. In light of that, when we looked at Linklogis (HKG:9959) and its ROCE trend, we weren't exactly thrilled.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Linklogis is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.032 = CN¥312m ÷ (CN¥12b - CN¥2.0b) (Based on the trailing twelve months to December 2021).

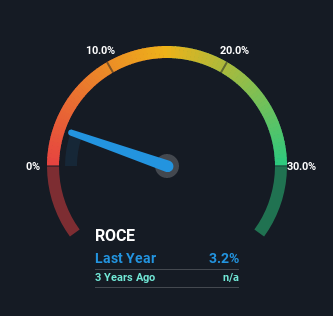

Thus, Linklogis has an ROCE of 3.2%. Ultimately, that's a low return and it under-performs the Software industry average of 6.2%.

See our latest analysis for Linklogis

SEHK:9959 Return on Capital Employed July 30th 2022

SEHK:9959 Return on Capital Employed July 30th 2022In the above chart we have measured Linklogis' prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Linklogis here for free.

So How Is Linklogis' ROCE Trending?

Over the past , Linklogis' ROCE and capital employed have both remained mostly flat. It's not uncommon to see this when looking at a mature and stable business that isn't re-investing its earnings because it has likely passed that phase of the business cycle. So unless we see a substantial change at Linklogis in terms of ROCE and additional investments being made, we wouldn't hold our breath on it being a multi-bagger.

What We Can Learn From Linklogis' ROCE

In a nutshell, Linklogis has been trudging along with the same returns from the same amount of capital over the last . And in the last year, the stock has given away 57% so the market doesn't look too hopeful on these trends strengthening any time soon. Therefore based on the analysis done in this article, we don't think Linklogis has the makings of a multi-bagger.

While Linklogis doesn't shine too bright in this respect, it's still worth seeing if the company is trading at attractive prices. You can find that out with our FREE intrinsic value estimation on our platform.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.