Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Andon Health Co., Ltd. (SZSE:002432) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Andon Health

How Much Debt Does Andon Health Carry?

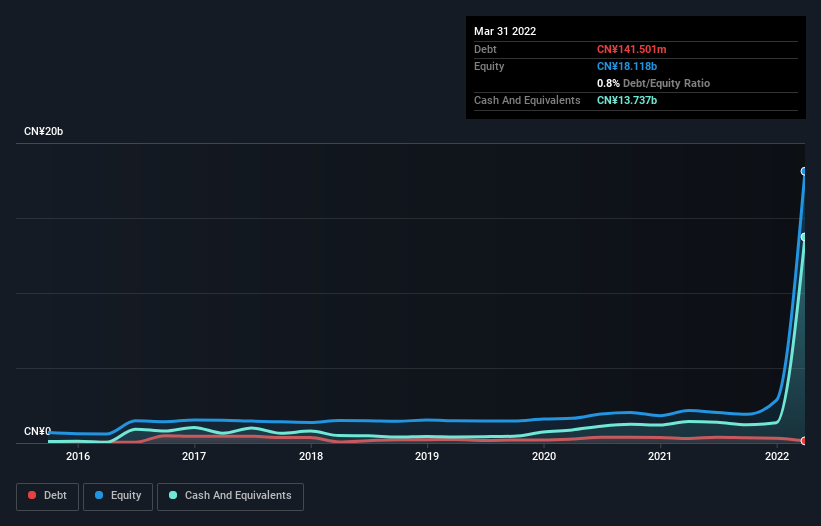

As you can see below, Andon Health had CN¥141.5m of debt at March 2022, down from CN¥303.2m a year prior. However, it does have CN¥13.7b in cash offsetting this, leading to net cash of CN¥13.6b.

SZSE:002432 Debt to Equity History July 6th 2022

SZSE:002432 Debt to Equity History July 6th 2022How Strong Is Andon Health's Balance Sheet?

The latest balance sheet data shows that Andon Health had liabilities of CN¥2.28b due within a year, and liabilities of CN¥51.3m falling due after that. Offsetting these obligations, it had cash of CN¥13.7b as well as receivables valued at CN¥4.31b due within 12 months. So it actually has CN¥15.7b more liquid assets than total liabilities.

This surplus strongly suggests that Andon Health has a rock-solid balance sheet (and the debt is of no concern whatsoever). On this view, lenders should feel as safe as the beloved of a black-belt karate master. Succinctly put, Andon Health boasts net cash, so it's fair to say it does not have a heavy debt load!

Better yet, Andon Health grew its EBIT by 4,615% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Andon Health will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Andon Health has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last two years, Andon Health produced sturdy free cash flow equating to 73% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing up

While it is always sensible to investigate a company's debt, in this case Andon Health has CN¥13.6b in net cash and a decent-looking balance sheet. And we liked the look of last year's 4,615% year-on-year EBIT growth. At the end of the day we're not concerned about Andon Health's debt. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example Andon Health has 3 warning signs (and 1 which is potentially serious) we think you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.