-

市场

-

产品

-

资讯

-

Moo社区

-

课堂

-

查看更多

-

功能介绍

-

费用费用透明,无最低余额限制

投资选择、功能介绍、费用相关信息由Moomoo Financial Inc.提供

- English

- 中文繁體

- 中文简体

- 深色

- 浅色

Analysts Have Been Trimming Their HUYA Inc. (NYSE:HUYA) Price Target After Its Latest Report

Analysts Have Been Trimming Their HUYA Inc. (NYSE:HUYA) Price Target After Its Latest Report

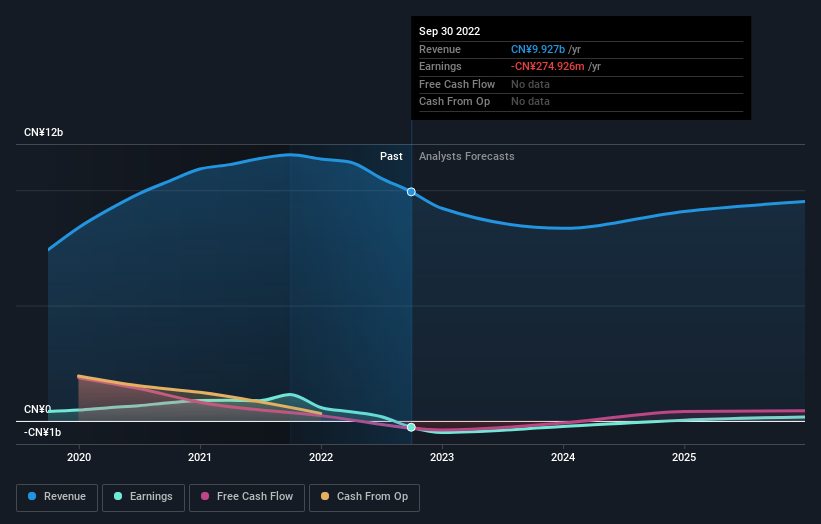

It's been a mediocre week for HUYA Inc. (NYSE:HUYA) shareholders, with the stock dropping 16% to US$3.31 in the week since its latest full-year results. Sales hit CN¥9.2b in line with forecasts, although the company reported a statutory loss per share of CN¥2.02 that was somewhat smaller than the analysts expected. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

See our latest analysis for HUYA

Taking into account the latest results, the current consensus, from the 13 analysts covering HUYA, is for revenues of CN¥8.27b in 2023, which would reflect a considerable 10% reduction in HUYA's sales over the past 12 months. Losses are predicted to fall substantially, shrinking 69% to CN¥0.64. Before this latest report, the consensus had been expecting revenues of CN¥8.57b and CN¥0.94 per share in losses. Although the revenue estimates have fallen somewhat, HUYA'sfuture looks a little different to the past, with a very favorable reduction to the loss per share forecasts in particular.

The consensus price target fell 7.0% to US$5.14, with the dip in revenue estimates clearly souring sentiment, despite the forecast reduction in losses. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values HUYA at US$9.86 per share, while the most bearish prices it at US$2.36. With such a narrow range of valuations, the analysts apparently share similar views on what they think the business is worth.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the HUYA's past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 10% by the end of 2023. This indicates a significant reduction from annual growth of 23% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 8.5% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - HUYA is expected to lag the wider industry.

The Bottom Line

The most obvious conclusion is that the analysts made no changes to their forecasts for a loss next year. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. Even so, long term profitability is more important for the value creation process. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

With that in mind, we wouldn't be too quick to come to a conclusion on HUYA. Long-term earnings power is much more important than next year's profits. We have forecasts for HUYA going out to 2025, and you can see them free on our platform here.

It is also worth noting that we have found 1 warning sign for HUYA that you need to take into consideration.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

It's been a mediocre week for HUYA Inc. (NYSE:HUYA) shareholders, with the stock dropping 16% to US$3.31 in the week since its latest full-year results. Sales hit CN¥9.2b in line with forecasts, although the company reported a statutory loss per share of CN¥2.02 that was somewhat smaller than the analysts expected. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

对于我来说,这是平庸的一周 HUYA Inc. 纽约证券交易所代码:HUYA)的股东,自最新全年业绩公布以来,该股本周下跌了16%,至3.31美元。销售额达到92亿人民币,符合预期,尽管该公司报告的法定每股亏损为2.02元人民币,略低于分析师的预期。结果公布后,分析师更新了盈利模型,最好知道他们是否认为公司的前景发生了重大变化,或者是否一切照旧。根据这些结果,我们收集了最新的法定预测,以了解分析师是否改变了收益模型。

See our latest analysis for HUYA

查看我们对 HUYA 的最新分析

Taking into account the latest results, the current consensus, from the 13 analysts covering HUYA, is for revenues of CN¥8.27b in 2023, which would reflect a considerable 10% reduction in HUYA's sales over the past 12 months. Losses are predicted to fall substantially, shrinking 69% to CN¥0.64. Before this latest report, the consensus had been expecting revenues of CN¥8.57b and CN¥0.94 per share in losses. Although the revenue estimates have fallen somewhat, HUYA'sfuture looks a little different to the past, with a very favorable reduction to the loss per share forecasts in particular.

考虑到最新业绩,涵盖HUYA的13位分析师目前的共识是,2023年的收入为827亿元人民币,这将反映出HUYA在过去12个月中销售额大幅减少了10%。预计损失将大幅下降,收缩69%,至0.64元人民币。在最新报告发布之前,人们普遍预计收入为85.7亿元人民币,每股亏损0.94元人民币。尽管收入估计有所下降,但Huya的未来看起来与过去略有不同,尤其是每股亏损预测的下降幅度非常可观。

The consensus price target fell 7.0% to US$5.14, with the dip in revenue estimates clearly souring sentiment, despite the forecast reduction in losses. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values HUYA at US$9.86 per share, while the most bearish prices it at US$2.36. With such a narrow range of valuations, the analysts apparently share similar views on what they think the business is worth.

共识目标价下跌7.0%,至5.14美元,尽管预计亏损将减少,但收入预期的下降显然使市场情绪恶化。查看分析师估计值的范围,评估异常值意见与均值的不同也可能很有启发性。目前,最看涨的分析师将HUYA估值为每股9.86美元,而最看跌的分析师将其估值为2.36美元。在估值范围如此狭窄的情况下,分析师显然对他们认为该业务的价值有相似的看法。

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the HUYA's past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 10% by the end of 2023. This indicates a significant reduction from annual growth of 23% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 8.5% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - HUYA is expected to lag the wider industry.

这些估计很有趣,但在观察预测与HUYA过去的表现和同行业同行的比较时,可以更宽泛地描绘一些概念。这些估计表明,预计销售将放缓,预计到2023年底,年化收入将下降10%。这表明比过去五年23%的年增长率大幅下降。相比之下,我们的数据表明,预计在可预见的将来,同一行业的其他公司(有分析师覆盖范围)的收入将每年增长8.5%。因此,尽管预计其收入将萎缩,但这种阴云并没有一线希望——预计HUYA将落后于整个行业。

The Bottom Line

底线

The most obvious conclusion is that the analysts made no changes to their forecasts for a loss next year. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. Even so, long term profitability is more important for the value creation process. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

最明显的结论是,分析师没有改变他们对明年亏损的预测。不利的一面是,他们还下调了收入预期,预测表明收入的表现将比整个行业差。即便如此,长期盈利能力对于价值创造过程更为重要。此外,分析师还下调了目标价格,这表明最新消息导致人们对该业务的内在价值更加悲观。

With that in mind, we wouldn't be too quick to come to a conclusion on HUYA. Long-term earnings power is much more important than next year's profits. We have forecasts for HUYA going out to 2025, and you can see them free on our platform here.

考虑到这一点,我们不会很快就HUYA得出结论。长期盈利能力比明年的利润重要得多。我们对HUYA的预测将持续到2025年,你可以在这里在我们的平台上免费看到它们。

It is also worth noting that we have found 1 warning sign for HUYA that you need to take into consideration.

还值得注意的是,我们已经发现 HUYA 有 1 个警告标志 这是你需要考虑的。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧? 取得联系 直接和我们联系。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St 的这篇文章本质上是一般性的。 我们仅使用不偏不倚的方法根据历史数据和分析师预测提供评论,我们的文章并非旨在提供财务建议。 它不构成买入或卖出任何股票的建议,也没有考虑您的目标或财务状况。我们的目标是为您提供由基本面数据驱动的长期重点分析。请注意,我们的分析可能未将最新的价格敏感型公司公告或定性材料考虑在内。简而言之,华尔街对上述任何股票都没有头寸。

moomoo是Moomoo Technologies Inc.公司提供的金融信息和交易应用程序。

在美国,moomoo上的投资产品和服务由Moomoo Financial Inc.提供,一家受美国证券交易委员会(SEC)监管的持牌主体。 Moomoo Financial Inc.是金融业监管局(FINRA)和证券投资者保护公司(SIPC)的成员。

在新加坡,moomoo上的投资产品和服务是通过Moomoo Financial Singapore Pte. Ltd.提供,该公司受新加坡金融管理局(MAS)监管(牌照号码︰CMS101000) ,持有资本市场服务牌照 (CMS) ,持有财务顾问豁免(Exempt Financial Adviser)资质。本内容未经新加坡金融管理局的审查。

在澳大利亚,moomoo上的金融产品和服务是通过Futu Securities (Australia) Ltd提供,该公司是受澳大利亚证券和投资委员会(ASIC)监管的澳大利亚金融服务许可机构(AFSL No. 224663)。请阅读并理解我们的《金融服务指南》、《条款与条件》、《隐私政策》和其他披露文件,这些文件可在我们的网站 https://www.moomoo.com/au中获取。

在加拿大,通过moomoo应用提供的仅限订单执行的券商服务由Moomoo Financial Canada Inc.提供,并受加拿大投资监管机构(CIRO)监管。

在马来西亚,moomoo上的投资产品和服务是通过Futu Malaysia Sdn. Bhd. 提供,该公司受马来西亚证券监督委员会(SC)监管(牌照号码︰eCMSL/A0397/2024) ,持有资本市场服务牌照 (CMSL) 。本内容未经马来西亚证券监督委员会的审查。

Moomoo Technologies Inc., Moomoo Financial Inc., Moomoo Financial Singapore Pte. Ltd., Futu Securities (Australia) Ltd, Moomoo Financial Canada Inc.,和Futu Malaysia Sdn. Bhd.是关联公司。

风险及免责提示

moomoo是Moomoo Technologies Inc.公司提供的金融信息和交易应用程序。

在美国,moomoo上的投资产品和服务由Moomoo Financial Inc.提供,一家受美国证券交易委员会(SEC)监管的持牌主体。 Moomoo Financial Inc.是金融业监管局(FINRA)和证券投资者保护公司(SIPC)的成员。

在新加坡,moomoo上的投资产品和服务是通过Moomoo Financial Singapore Pte. Ltd.提供,该公司受新加坡金融管理局(MAS)监管(牌照号码︰CMS101000) ,持有资本市场服务牌照 (CMS) ,持有财务顾问豁免(Exempt Financial Adviser)资质。本内容未经新加坡金融管理局的审查。

在澳大利亚,moomoo上的金融产品和服务是通过Futu Securities (Australia) Ltd提供,该公司是受澳大利亚证券和投资委员会(ASIC)监管的澳大利亚金融服务许可机构(AFSL No. 224663)。请阅读并理解我们的《金融服务指南》、《条款与条件》、《隐私政策》和其他披露文件,这些文件可在我们的网站 https://www.moomoo.com/au中获取。

在加拿大,通过moomoo应用提供的仅限订单执行的券商服务由Moomoo Financial Canada Inc.提供,并受加拿大投资监管机构(CIRO)监管。

在马来西亚,moomoo上的投资产品和服务是通过Futu Malaysia Sdn. Bhd. 提供,该公司受马来西亚证券监督委员会(SC)监管(牌照号码︰eCMSL/A0397/2024) ,持有资本市场服务牌照 (CMSL) 。本内容未经马来西亚证券监督委员会的审查。

Moomoo Technologies Inc., Moomoo Financial Inc., Moomoo Financial Singapore Pte. Ltd., Futu Securities (Australia) Ltd, Moomoo Financial Canada Inc.,和Futu Malaysia Sdn. Bhd.是关联公司。

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用浏览器的分享功能,分享给你的好友吧