-

市场

-

产品

-

资讯

-

Moo社区

-

课堂

-

查看更多

-

功能介绍

-

费用费用透明,无最低余额限制

投资选择、功能介绍、费用相关信息由Moomoo Financial Inc.提供

- English

- 中文繁體

- 中文简体

- 深色

- 浅色

Hutchison Port Holdings Trust (SGX:NS8U) Seems To Use Debt Quite Sensibly

Hutchison Port Holdings Trust (SGX:NS8U) Seems To Use Debt Quite Sensibly

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Hutchison Port Holdings Trust (SGX:NS8U) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Hutchison Port Holdings Trust

What Is Hutchison Port Holdings Trust's Net Debt?

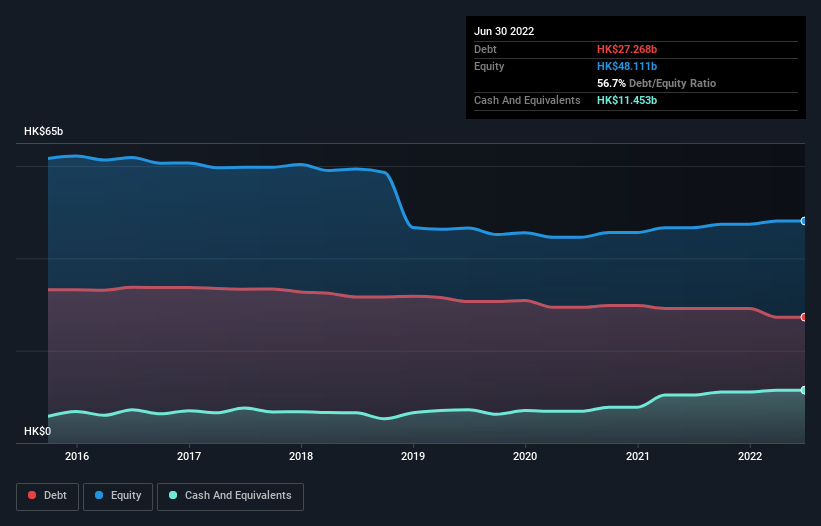

As you can see below, Hutchison Port Holdings Trust had HK$27.3b of debt at June 2022, down from HK$29.1b a year prior. However, it does have HK$11.5b in cash offsetting this, leading to net debt of about HK$15.8b.

SGX:NS8U Debt to Equity History September 26th 2022

SGX:NS8U Debt to Equity History September 26th 2022How Strong Is Hutchison Port Holdings Trust's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Hutchison Port Holdings Trust had liabilities of HK$16.6b due within 12 months and liabilities of HK$27.1b due beyond that. On the other hand, it had cash of HK$11.5b and HK$4.23b worth of receivables due within a year. So its liabilities total HK$28.0b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the HK$13.6b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Hutchison Port Holdings Trust would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With a debt to EBITDA ratio of 2.3, Hutchison Port Holdings Trust uses debt artfully but responsibly. And the fact that its trailing twelve months of EBIT was 9.7 times its interest expenses harmonizes with that theme. If Hutchison Port Holdings Trust can keep growing EBIT at last year's rate of 14% over the last year, then it will find its debt load easier to manage. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Hutchison Port Holdings Trust can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Happily for any shareholders, Hutchison Port Holdings Trust actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Hutchison Port Holdings Trust's level of total liabilities was a real negative on this analysis, although the other factors we considered were considerably better. In particular, we are dazzled with its conversion of EBIT to free cash flow. We would also note that Infrastructure industry companies like Hutchison Port Holdings Trust commonly do use debt without problems. Looking at all this data makes us feel a little cautious about Hutchison Port Holdings Trust's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Hutchison Port Holdings Trust (at least 1 which is potentially serious) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

伯克希尔哈撒韦的外部基金经理理想汽车·卢直言不讳地说,最大的投资风险不是价格的波动,而是你是否会遭受永久性的资本损失。当你考察一家公司的风险有多大时,考虑它的资产负债表是很自然的,因为当一家企业倒闭时,债务往往会涉及到它。与许多其他公司一样和记港口控股信托基金(SGX:NS8U)利用债务。但股东是否应该担心它的债务使用情况?

债务在什么时候是危险的?

一般来说,只有当一家公司无法轻松偿还债务时,债务才会成为一个真正的问题,无论是通过筹集资金还是用自己的现金流。资本主义的一部分是“创造性破坏”的过程,破产的企业被银行家无情地清算。尽管这并不常见,但我们确实经常看到负债累累的公司永久性地稀释股东的权益,因为贷款人迫使他们以令人沮丧的价格筹集资金。然而,通过取代稀释,对于需要资本投资于高回报率增长的企业来说,债务可以成为一个非常好的工具。当我们考虑一家公司的债务用途时,我们首先会把现金和债务放在一起看。

查看我们对和记港口控股信托的最新分析

和记黄埔港口控股信托的净债务是多少?

如下所示,截至2022年6月,和记黄埔港口控股信托的债务为273亿港元,低于一年前的291亿港元。然而,它确实有115亿港元的现金抵消了这一影响,导致净债务约为158亿港元。

新交所:NS8U债转股历史2022年9月26日和记黄埔港口控股信托的资产负债表有多强劲?

放大最新的资产负债表数据,我们可以看到和记港口控股信托有166亿港元的负债在12个月内到期,还有271亿港元的负债在12个月内到期。另一方面,该公司有115亿港元的现金和价值42.3亿港元的应收账款在一年内到期。因此,该公司的负债总额比现金和短期应收账款的总和高出280亿港元。

这一赤字给这家市值136亿港元的公司蒙上了一层阴影,就像一个庞然大物耸立在凡人之上。因此,毫无疑问,我们会密切关注它的资产负债表。归根结底,如果债权人要求偿还,和记黄埔港口控股信托公司可能需要进行大规模的资本重组。

我们通过查看公司的净债务除以利息、税项、折旧和摊销前收益(EBITDA),并计算其息税前收益(EBIT)覆盖利息支出(利息覆盖)的容易程度,来衡量公司的债务负担与其盈利能力的关系。这样,我们既考虑了债务的绝对量,也考虑了为其支付的利率。

和记港口控股信托的债务与EBITDA之比为2.3,该公司巧妙但负责任地使用债务。它过去12个月的息税前利润是利息支出的9.7倍,这一事实与这一主题相一致。如果和记港口控股信托能够保持去年14%的息税前利润增速,那么它将发现自己的债务负担更容易管理。在分析债务水平时,资产负债表显然是一个起点。但最终,该业务未来的盈利能力将决定和记黄埔港口控股信托能否随着时间的推移加强其资产负债表。所以,如果你关注未来,你可以看看这个免费显示分析师利润预测的报告。

最后,企业需要自由现金流来偿还债务;会计利润只是不能削减这一点。因此,合乎逻辑的一步是看看息税前利润与实际自由现金流相匹配的比例。对于任何股东来说,令人高兴的是,和记黄埔港口控股信托在过去三年产生的自由现金流实际上超过了息税前利润。这种强大的摇钱树就像一只穿着大黄蜂西装的小狗一样温暖着我们的心。

我们的观点

和记港口控股信托的总负债水平在这一分析中确实是负面的,尽管我们考虑的其他因素要好得多。特别是,它将息税前利润转换为自由现金流,让我们眼花缭乱。我们还将注意到,像和记黄埔这样的基础设施行业公司通常会使用债务,而不会出现问题。看着所有这些数据,我们对和记港口控股信托的债务水平感到有点谨慎。虽然债务确实有更高的潜在回报,但我们认为股东绝对应该考虑债务水平可能会如何使股票的风险更高。在分析债务水平时,资产负债表显然是一个起点。但归根结底,每家公司都可能包含存在于资产负债表之外的风险。我们已经确定了两个警告信号与和记黄埔港口控股信托基金(至少1家,这可能是严重的),并了解他们应该是你的投资过程的一部分。

当然,如果你是那种喜欢在没有债务负担的情况下购买股票的投资者,那么不要犹豫,今天就来看看我们的净现金成长型股票独家名单。

对这篇文章有什么反馈吗?担心内容吗? 保持联系直接与我们联系。或者,也可以给编辑组发电子邮件,地址是implywallst.com。

本文由Simply Wall St.撰写,具有概括性。我们仅使用不偏不倚的方法提供基于历史数据和分析师预测的评论,我们的文章并不打算作为财务建议。它不构成买卖任何股票的建议,也没有考虑你的目标或你的财务状况。我们的目标是为您带来由基本面数据驱动的长期重点分析。请注意,我们的分析可能不会将最新的对价格敏感的公司公告或定性材料考虑在内。Simply Wall St.对上述任何一只股票都没有持仓。

moomoo是Moomoo Technologies Inc.公司提供的金融信息和交易应用程序。

在美国,moomoo上的投资产品和服务由Moomoo Financial Inc.提供,一家受美国证券交易委员会(SEC)监管的持牌主体。 Moomoo Financial Inc.是金融业监管局(FINRA)和证券投资者保护公司(SIPC)的成员。

在新加坡,moomoo上的投资产品和服务是通过Moomoo Financial Singapore Pte. Ltd.提供,该公司受新加坡金融管理局(MAS)监管(牌照号码︰CMS101000) ,持有资本市场服务牌照 (CMS) ,持有财务顾问豁免(Exempt Financial Adviser)资质。本内容未经新加坡金融管理局的审查。

在澳大利亚,moomoo上的金融产品和服务是通过Futu Securities (Australia) Ltd提供,该公司是受澳大利亚证券和投资委员会(ASIC)监管的澳大利亚金融服务许可机构(AFSL No. 224663)。请阅读并理解我们的《金融服务指南》、《条款与条件》、《隐私政策》和其他披露文件,这些文件可在我们的网站 https://www.moomoo.com/au中获取。

在加拿大,通过moomoo应用提供的仅限订单执行的券商服务由Moomoo Financial Canada Inc.提供,并受加拿大投资监管机构(CIRO)监管。

在马来西亚,moomoo上的投资产品和服务是通过Futu Malaysia Sdn. Bhd. 提供,该公司受马来西亚证券监督委员会(SC)监管(牌照号码︰eCMSL/A0397/2024) ,持有资本市场服务牌照 (CMSL) 。本内容未经马来西亚证券监督委员会的审查。

Moomoo Technologies Inc., Moomoo Financial Inc., Moomoo Financial Singapore Pte. Ltd., Futu Securities (Australia) Ltd, Moomoo Financial Canada Inc.,和Futu Malaysia Sdn. Bhd.是关联公司。

风险及免责提示

moomoo是Moomoo Technologies Inc.公司提供的金融信息和交易应用程序。

在美国,moomoo上的投资产品和服务由Moomoo Financial Inc.提供,一家受美国证券交易委员会(SEC)监管的持牌主体。 Moomoo Financial Inc.是金融业监管局(FINRA)和证券投资者保护公司(SIPC)的成员。

在新加坡,moomoo上的投资产品和服务是通过Moomoo Financial Singapore Pte. Ltd.提供,该公司受新加坡金融管理局(MAS)监管(牌照号码︰CMS101000) ,持有资本市场服务牌照 (CMS) ,持有财务顾问豁免(Exempt Financial Adviser)资质。本内容未经新加坡金融管理局的审查。

在澳大利亚,moomoo上的金融产品和服务是通过Futu Securities (Australia) Ltd提供,该公司是受澳大利亚证券和投资委员会(ASIC)监管的澳大利亚金融服务许可机构(AFSL No. 224663)。请阅读并理解我们的《金融服务指南》、《条款与条件》、《隐私政策》和其他披露文件,这些文件可在我们的网站 https://www.moomoo.com/au中获取。

在加拿大,通过moomoo应用提供的仅限订单执行的券商服务由Moomoo Financial Canada Inc.提供,并受加拿大投资监管机构(CIRO)监管。

在马来西亚,moomoo上的投资产品和服务是通过Futu Malaysia Sdn. Bhd. 提供,该公司受马来西亚证券监督委员会(SC)监管(牌照号码︰eCMSL/A0397/2024) ,持有资本市场服务牌照 (CMSL) 。本内容未经马来西亚证券监督委员会的审查。

Moomoo Technologies Inc., Moomoo Financial Inc., Moomoo Financial Singapore Pte. Ltd., Futu Securities (Australia) Ltd, Moomoo Financial Canada Inc.,和Futu Malaysia Sdn. Bhd.是关联公司。

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用浏览器的分享功能,分享给你的好友吧