Riding the Recovery of the Construction Sector- Hock Lian Seng

$Hock Lian Seng(J2T.SG$ $Koh Bros(K75.SG$ $Lian Beng(L03.SG$ $FTSE Singapore Straits Time Index(.STI.SG$

With Covid 19 causing huge disruption to the economy, the construction sector was especially affected given the migrant workers' high infection rate. But, things are starting to look brighter, with the government getting things back to normalcy. With the 'Live with the covid Directive', most migrant workers will be able to go back to work as long as they get vaccinated.

With Covid 19 causing huge disruption to the economy, the construction sector was especially affected given the migrant workers' high infection rate. But, things are starting to look brighter, with the government getting things back to normalcy. With the 'Live with the covid Directive', most migrant workers will be able to go back to work as long as they get vaccinated.

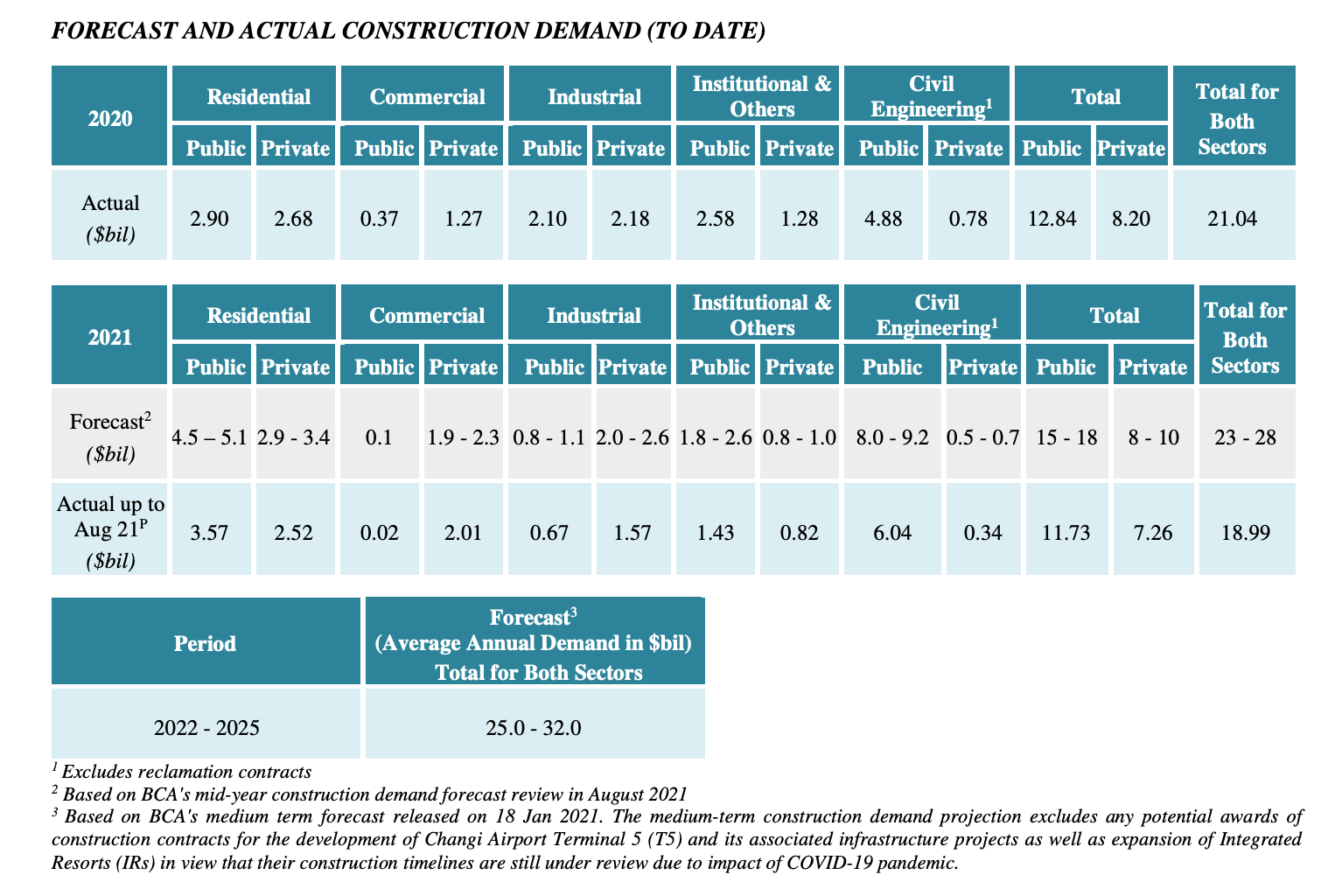

Given the BCA guidance, things are starting to be turning up based on the contracts awarded. You could find the latest Building and Construction Authority forecast appended below. This could be due to pent- up demand, given news of BTO delays. Moreover, the government's initiative to boost up infrastructure spending to jumpstart the economy post covid would also provide a further tailwind.

Source: BCA Media Release Jan 2021

Giving some context, the total contracts awarded in 2019 were in the region of 33 billion. The general forecasted contracts from 2014 to 2019 are also higher than the current forecasted contract values for the next few years.

Giving some context, the total contracts awarded in 2019 were in the region of 33 billion. The general forecasted contracts from 2014 to 2019 are also higher than the current forecasted contract values for the next few years.

But, things are moving rapidly and any forecast could be derailed or even surpassed. Nonetheless, one thing is for sure, the figures are likely going to be higher than 2020 which bore the full brunt of the pandemic.

Also, the trump card would be the contracts for Changi Airport Terminal 5 and the Integrated Resorts expansion, which have been excluded from the forecast.

Source: BCA Media Release Jan 2015

With this backdrop, we started to look into the construction companies in Singapore that could ride this recovery of the sector and provide meaningful returns in the midterm (1-3 years). Some names came into mind such as Lian Beng, which recently got a privatisation offer from the founding family at $0.5.

It is more of a formality (Low probability of being accepted given it is trading at Price to Book of 0.35) as they have increased their stake in the firm.

The other names would be Koh Brothers and OKP. Given the uncertainty of the recovery, we would prefer a safer company (No debt) with a good track record and is known to be a generous dividend payer in good times.

Hock Lian Seng

This brings us to shortlist Hock Lian Seng which was established in 1969. Hock Lian Seng is currently lingering near the recent lower range of their share price movements despite seeing an improvement in earnings. Here is a good summary by Morningstar of what Hock Lian Seng's business is involved in.

Source: Morningstar Business Description

Financial Metrics

We start our analysis by looking at some of their numbers:

Looking at the numbers, it is something that excites a value investor as their balance sheet is strong, and it is trading at a reasonable valuation. Taking away the cash and investment securities, we are looking at a profitable business that could be riding on an improvement in their sector at only 7 cents (0.23-0.16) or PE of around 3.33. The dividend yield is kind of disappointing but 2020 was a bad year after all.

Source: Hock Lian Seng June 2021 Financial Statements

From their latest half-yearly results, we are seeing a marked improvement in revenue and earnings that are growing in tandem. It points to the recovery thesis to be on track. The Group’s order book for ongoing projects of the civil engineering segment was approximately $308 million for the Maxwell station and the Changi Airport joint venture project as of June 2021.

Source: HLS 2020 Annual Report

From the figures extracted from the annual report, this is not a growth stock with consistent increment in revenue and profits but is reflective of the cyclical business in which the construction sector is.

It is heartening to know that despite the huge drop in revenue for 2020, the company was still able to maintain profitability. This shows the acumen and strength of the management. Not forgetting the ability to tender wisely for projects given the rising construction cost from labour and raw materials.

Source: HLS 2020 Annual Report

One of the merits of this investment would be the management have been a believer in rewarding shareholders through generous dividends, as we could see from their track record through the years. We could be looking at a dividend of above 5% based on their distribution history if things go back to normalcy.

Chartist Point of View

Hock Lian Seng was listed in 2011 and the current share price is near the lowest it ever went to. The price action seems to be bottoming out which gives us a potential choice entry-level.

For potential targets, the 0.27-0.3 region will be the first resistance and target level. If things pan out well, 0.38-0.4 would be viable and supported by the fundamentals- their current PE of 3.33 based on ex-cash and investment securities is attractive.

A possible stop level could be placed below 0.2 if it is a purely trading play.

Summing Up

The following pointers sum up our thoughts on Hock Lian Seng as a proxy to ride the recovery of Singapore's construction sector.

1) The construction sector is picking up from the Covid 19 effect and we have seen an increase in total contracts value from 2020 to 2021. Forecasted contract values to 2025 are expected to move up further from the current status.

2) Valuation seems attractive for Hock Lian Seng and there was a marked improvement in their revenue and earnings based on their half-yearly results.

3) A big portion of the current market cap is backed by cash and investment securities- give us a good margin of safety.

4) It has a good track record of being a good dividend yield stock and has been profitable every year since listing.

5) Finally, Charting Perspective looks decent as it is coming up from the lower end of the price range since listing.

Disclaimer: Community is offered by Moomoo Technologies Inc. and is for educational purposes only.

Read more

Comment

Sign in to post a comment

Celestinel : $APHLF I had $STIwhen it was an OTC. It was .53 and I had 2500 of shares. I never added and sold it at about $2. 2 mistakes. Never added to it as I should have and sold too early.

I will not make that mistake with APHLF.